Tag: retirement

Kevin O’Leary: Why Early Retirement Doesn’t Work

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

This whole idea of financial independence retire early doesn't work. Let me tell you why. It happened to me. On the sale of my

first company, I achieved great liquidity and I

thought to myself, "Hey. I'm 36. I can retire now." I retired for three years. I was bored out of my mind. Working is not

just about money. People don't understand this very

often until they stop working.

Work defines who you are. It provides a place where

you're social with people. It gives you interaction with people

all day long in an interesting way. It even helps you live longer

and is very, very good for brain health. Staying stimulated is how people

live into their 90s. I'm not kidding. So when am I retiring? Never. Never. I don't know where I'm going

after I'm dead, but I'll be working when I get there too..

10 Levels of Financial Independence And Early Retirement | How to Retire Early

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Long-term financial goals can sometimes seem

so big that they feel almost unattainable especially when we’re just getting started

on our road to financial independence. I and many others like me in the financially

independent, retired early community have found it helpful to break down the goal of

becoming financially independent into smaller and more manageable levels of financial independence. Not only because it makes it easier for us

to track our progress, which in turns helps us to stay motivated throughout the process,

but also because it helps us get over that initial hurdle of starting to chip away at

this mountain of a task. In today’s video, I’m going to take you

through what I consider to be the 10 levels of financial independence as well as give

an example on how to go from the first level to the top level in your lifetime. Hey everyone Daniel here and welcome to Next

Level Life a channel where you can learn about Investing, debt, retirement, and many other

general financial education videos because the school's aren't going to do it for us.

So if any of those topics sound interesting

to you or if you want to learn how to better handle your money and have more financial

freedom be sure to hit that subscribe button and the bell next to my name to be notified

every time I upload a video. And if you want to further support the growth

of this channel you can check out some of the links I’ve left down in the description

below which includes a 30-day free trial of Audible and 2 free audiobooks of your choice

as well as a list of some books on money I’d recommend checking out, or you can share this

video with a friend, and leave a comment below letting me know what topics you’d like me

to cover in future videos.

Now obviously these ideas of the levels of

financial independence are not solely my own nor are they very new as there are many articles

and blog posts that have covered this topic already and have done so for many years. So consider this more of a summary of many

of the ideas expressed in those articles and if you want to learn more about the topic

feel free to check out some of the articles for yourself. I’ve left some links in the description. With that out of the way, let’s get started. Okay so real quick the 10 levels of financial

Independence are Level 0 Financial dependence, level 1 Financial solvency, level 2 Financial

stability, level 3 debt Freedom, level four coasting Financial Independence (also sometimes

known as freedom from employer), level 5 Financial Security, level six Financial flexibility,

level 7 Financial independence, level eight Financial Freedom, and finally level 9 Financial

abundance. The levels are usually defined as something

like the following: Level 0 – Financial dependency is when your

debt payments and other living expenses are greater than your own income.

This means that you are in one way or another

dependent on someone or something else to help you pay for your bills or if you happen

to be a kid and don't actually have any bills you need someone else, usually your parents,

to pay to put food on the table and keep the lights on and have a roof over your head. This is the level that all of us start out

on and it is referred to as level 0 because as a financial dependent you obviously have

no Financial Independence. Level 1 – Financial solvency is when you are

current on all your debt payments and you can meet your financial commitments and your

other living expenses without any outside help. Level 2 – Financial stability is usually defined

as when you have built some sort of emergency fund in addition to being financially solvent. Level 3 – Is again debt freedom and it's defined

differently depending on who you ask. For some, it is being completely debt-free,

mortgage and everything.

For others, it's being just free of the high-interest

debts like credit cards but you still might have a mortgage or other debts like student

loans. And for some others, it is paying off all

of your debts except for the mortgage but your credit cards and student loans or car

loans all that stuff is all paid off. Level 4 – Coasting Financial Independence

also sometimes known as freedom from the employer, Barista Financial Independence, or Agency

in blogs and other mediums. I personally like the idea of it being coasting

Financial Independence so that's what I'm going to be using in this video but know that

some people refer to it by one of those other titles but the idea is the same. You have reached the level of coasting Financial

Independence when you could, if you wanted to, step down from a job that may be higher-paying

but may also be either less satisfying or more stressful or both into a new job that

is lower paying but more enjoyable or less stressful or both.

This is because in the early years of your

career or just thought most recent years you have managed to save a very decent sum of

money that would be able to provide for the later years of your retirement after it has

grown even if you don't put much more in. Therefore all you need to do is make enough

money to get you to age 60 or 65 or 70 or whatever your numbers work out to be when

that amount of money you've already invested will be able to fund your lifestyle because

it's been given enough time to grow. So in a sense, you've worked really really

hard and been very frugal in the first few years so that you can coast into your retirement. I have gone into more detail on the various

types of financial Independence in a previous video which I'll leave Linked In the description

if you're interested in learning more.

Level 5 – Financial Security is effectively

when your cash flow from wealth such as you are investments has grown to large enough

that it can provide for your annual basic survival expenses. Now I say survival expenses because I do differentiate

that from living expenses survival expenses are just the basic things you need to survive

Food, Water, Shelter, some form of transportation, clothing and probably insurance. This does not include things like Netflix

subscriptions or cable bills or things like that it is purely survival expenses. So this may not be exactly the ideal spot

to retire and I certainly wouldn't want to retire at this point but it is an important

level to keep in mind because it does give you… well security. If you were to get fired today and you were

on level 5 you would be okay you could survive until you found another job. This is essentially the first level that really

gives you I guess that piece of mind even if the lifestyle should you have chosen to

live it may not be the most lavish.

Level 6 – Financial flexibility is similar

to Financial Security just one step up. It is when you have the ability to live off

of your current cash flow from your wealth assuming that you have a flexible spending

plan that adjusts for up and downs in the market. So if the markets up 20% one year you're able

to spend a little bit more but if the market is down 20% the next year then you don't spend

quite as much. I’ve seen it defined many different ways

so it could vary depending on who you ask, but the one that I personally like the most

is that it is roughly half of your full financial independence goal, or roughly about 12.5x

your current annual expenses if you follow the 4% rule to get an idea of how much money

you need to retire like I’ve explained in previous videos.

So it isn't quite Financial Independence yet

but it's close. Level 7 – Is financial Independence and it's

usually based on the 4% rule which I have covered in a previous video. You can follow the 4% rule when you have saved

roughly 25x your annual expenses. The vast majority of the time this will be

enough money to allow you to maintain your current lifestyle in retirement and as a result,

you can be considered financially independent. And some articles end it right there but I

think there are a couple of levels that are a bit higher than that that are worth considering

even if some of us may decide to not ever try to achieve them because being at level

7 allows them to do what they wanted all along. So let's talk about those other levels. Level 8 – Is Financial Freedom which I've

often seen defined as the cash flow from your Investments is greater than financial Independence

and a few more life goals.

Life goals, of course, will differ for everybody

but this is could be something like taking a trip or two overseas or moving to a new

place you've always wanted to live but haven't had quite enough money to live there up till

now or whatever the case may be for you like I said it's different for everybody. Level 9 – Is financial abundance and this

is quite simply just that the cash flow from your Investments is more than you will ever

need.

You could spend it if you really wanted to

but it would actually take some effort. And the stuff from level 8 doesn't really

cut into it much at all. So you could up those goals even more and

still have more cash flow left over at the end of the year. This also probably has a slightly different

definition for each person depending on who you ask, but I like to think of it as roughly

3x your financial freedom number because this would allow you to experience a horrible bear

market where your investments go down by 50% and still has 1.5x the amount that you would

need to maintain the lifestyle you lead when you reach level 8.

To me, that means that it is likely more than

you will ever need, but again that one is strictly my own opinion on the matter. So those are the 10 levels of financial Independence,

now let's walk through a hypothetical example of how someone could go from Level 0 to being

financially independent in a single lifetime. John and Jane are recently married couple

each making $20 an hour at age 23 or $83,200 a year between them assuming no overtime. They manage this because they are not only

good hard-working people but got great grades in school and we're selective about the job

that they decided to pursue. Obviously just like everyone else they would

have started off as Financial dependents and as they were going through college they would

have been building up student loans that they would not have had the money to pay off (assuming

of course that they didn't earn enough money while in school to keep up with the rising

debt).

In all they have credit card debt, two car

payments and the student loans which have balances of $5,000, $35,000, and $60,000 respectively,

but since they got their jobs they are no longer financially dependent and their incomes

have allowed them to become current on all their debt payments without the help of others. In addition to the regular monthly debt payments,

their annual expenses are $48,000 a year. So they are currently in level one Financial

solvency and trying to figure out a way to move to level 2 Financial stability. In order to do that they need to figure out

a way to build up an emergency fund.

Now if they're following the 10 levels system

to a T then they would look to build a 3 to 6-month emergency fund of their survival expenses. However, this is not the only way to approach

it say if you were to follow Dave Ramsey 7 baby steps you would start off with just a

$1,000 starter emergency fund and then get right onto attacking your debts. And other Financial systems and plans may

have you approached it an entirely different way.

Either way is perfectly fine because the 10

levels system is not meant to be a financial formula per say it's more there to give us

some sort of guidepost so that we can better track our progress towards achieving Financial

Independence. But for the purposes of this video, I am going

to assume that they follow the 10 levels in order so we are going to be building up a

full emergency fund. In order to find how much of an emergency

fund they will need we will need to know how much money they need to survive not necessarily

on their current level of expenses while they have jobs but purely on Survival expenses

which are basically your four walls of your financial house or in other words food shelter

including utilities Basic clothing and some form of transportation as well as the insurances

that are related to that assuming there are any.

In this case, I'm going to assume that their

survival expenses are right around $3,000 a month. Which means that in order to get a 3-month

emergency fund they would need $9,000 in order to get a six-month emergency fund they would

need to save $18,000. Both John and Jane feel that their jobs are

pretty darn secure and the market is doing fairly well so it's not likely at least in

the near-term that they would get laid off because the company has to downsize so they

decide together that they are comfortable with having just a 3-month emergency fund

of $9,000. So with $83,200 a year in income, $48,000

a year and expenses, plus minimum monthly payments of $100 on the credit card which

is 2% of the balance, $550.78 on the car loans, and $621.83 on the student loans they will

have approximately $1,660.72 a month left over to start building their emergency fund.

However, both John and Jane have been looking

into their finances and researching a lot lately and they become fired up at the possibility

of becoming financially independent while they're still young. So they want to see if there's a way that

they can speed this whole process up. And as it turns out thankfully there are many. After taking a look at the options they decide

that they're going to work as much overtime as they possibly can (for the sake of Simplicity

I'm going to assume that they manage to work on average 5 hours per week of overtime which

will increase their monthly income by about $1,300 a month, meaning that instead of $1,660

a month they will have $2,960 a month left over) and they're going to sell both of their

cars and buy some nice used cars with cash to help knock down some of that initial debt. After putting out a couple of ads online they

managed to find buyers for each of their cars that is willing to give them $15,000.

So they take that $30,000 and use $5,000 of

it to pay off the credit card balance and another $10,000 to buy a couple of used cars

from someone that they know takes good care of their Vehicles whether that be a family

friend or just a mechanic that they Trust. The remaining $15,000 is thrown at their car

loans. This means that the credit card loan is fully

paid off and therefore the hundred-dollar minimum payment is no longer needed. So John and Jane start throwing $3,060 per

month into their emergency fund and get it fully funded in 3 months with a little bit

left over at the end of the third month to throw out their car loan. Over the course of those first three months,

they managed to bring the car loans balances down to $18,423 thanks in large part to the

$15,000 that they threw at it in the first month after selling the cars and also making

the minimum payments in the first three months. Now that their emergency fund is fully funded

however they're able to throw that $3,060 a month in addition to the $550 a month minimum

payment at the car loan and get it paid off in 6 months flat.

So a mere nine months into their Journey John

and Jane not only have a fully funded emergency fund but they also have paid off both of their

car loans. Now there are just the student loans to tackle. And thanks to the fact that they've been making

minimum payments on them for 9 months and the fact that they had a little over $3,000

at the end of the ninth month after paying off their car loans their student loans now

have a balance of $53,263. John and Jane follow the same pattern that

they did with the car loans throwing the $3,600+ which is what they now have left over at the

end of every month because they no longer had a $550 car payment to make and they managed

to get their student loans paid off in full in 13 months. So John and Jane have managed to become debt

free and have a fully funded emergency fund in 22 months.

They have now reached level three and because

of that they now have over $4,200 a month left over to start investing. This brings us to level four coasting Financial

Independence. Let's assume that John and Jane want to retire

by the age of 65. That means that whatever they put in now needs

to be enough to grow to a point where it can support their lifestyle in retirement by the

time they're 65. If we assume a rate of return on an average

in the market of about 10% before inflation and an inflation rate of about 3% per year

on average then we can get a rough estimate of how much John and Jane need to put away

in order to achieve a state of coasting Financial Independence. In this case, since they're 24 about to be

25 they will have somewhere in the neighborhood of 39 or 40 years to let the money grow before

needing to take any of it out. If their expenses were $48,000 a year at age

23 then 42 years later if we assume a 3% rate of inflation they would need a tad bit over

$166,000 each year to live on.

Again assuming we follow the 4% rule to figure

out how much they need once they fully retire to be financially independent that means that

they would have to have at least $4.15 million invested in the market by the time they turn

65. In their case, they would need about $110,000

saved up give or take in order to achieve coasting Financial Independence and because

they're able to save about $4,233 a month now that they’re debt free, they’re able

to hit that goal in 2 years flat.

Meaning that in theory, they would be able

to step down from their jobs to a more rewarding less stressful but probably lower-paying job

just 3 years and 10 months into their financial Journey. That is incredible! But like I said coasting Financial Independence

wasn't their end goal. They wanted to be fully Financial Independent

so they keep working and investing for now. The next level is level 5 Financial Security

which is achieved when your cash flow from your Investments is greater than your annual

survival expenses which remember is $3,000 a month or $36,000 a year in John and James

case. Because they are debt-free, are making good

money at their jobs, and being intentional with their finances they Achieve Financial

Security in a little over 4 years with over $367,000 in their portfolio.

It is been a mere 87 months or 7 years and

3 months since they began their financial Journey. John and Jane are 30 years old and they are

able to get by on their Investments alone. In theory, they could retire now, it wouldn't

be the most glamorous retirement and it wasn't their goal but it is an option they have. They don't have to worry about losing their

jobs anymore because even if both of them lost their jobs today they would be able to

make it long enough to either find a new job or some other source of income. This is really the first level where you start

to get that piece of mind when it comes to money at least in my opinion. Next is financial flexibility which as I mentioned

earlier in the video has many definitions depending on who you ask but for the purposes

of this video, I'm assuming that it is roughly 12.5x your current annual expenses which for

John and Jane would be roughly $600,000 or about $855,000 if you account for inflation. This means that they would Achieve Financial

flexibility 9 years and 8 months into their Journey not accounting for inflation or about

11 years and 9 months if we do account for inflation.

John and Jane continue investing through all

the highs and lows of the markets until they reach Financial Independence exactly 14 years

into their financial Journey assuming we don't account for inflation or 18 years and 3 months

if we do. So you might be wondering why did I split

up the accounting for inflation time frames and the not accounting for inflation time

frames should we always be accounting for inflation? Well technically yes but the reason I split

them up is because in my experience taking this journey myself as well as seeing others

take it, this journey changes how you view a lot of things and more often than not those

changes lead to you valuing things such as freedom of mobility and location and freedom

of time to be able to spend with the people you love more and valuing more material things

that cost possibly a lot of money less and less. That's not to say that everybody becomes minimalist

going through this journey, I'm not saying that at all but I have seen a lot of people

who have gone through this journey become closer to minimalist than they were when they

started the journey as they find out more and more things that they used to buy just

don’t provide enough value or happiness for them to be worth the purchase.

They find better uses for their money and

time and as a result, they generally tend to spend less. Which means that even though inflation is

technically increasing your expenses by making every dollar less and less valuable over time,

if you're also decreasing your expenses because what you value is changing it may even out

or in some cases, you may even see your regular expenses going down year-over-year as you

continue through this journey. So that's why I split them up. And, before I go, I do want to mention that

based on what I've seen on various articles and forums some people really like to have

even more goals to chase as they go through this journey than what I've laid out today

in this video so if that's something that would help you feel free to break down these

levels even further then I have today this is obviously just the list that I used and

what worked for me, but you could take it even further.

For example, Debt Freedom could be broken

down into three separate stages: One where you are free from all high-interest debt,

a second where you are free from all debts except for the house (if you have one), and

a third where you are totally debt-free. You could tackle the coasting Financial Independence

level in a similar way breaking it down into two stages: One where are you have invested

enough to survive in retirement and a second where you have invested enough in order to

maintain your current lifestyle, adjusting for inflation of course, in retirement.

And the financial independence level could

also be broken down into three stages: Stage one would be where you are at a survivable

level of financial Independence, stage 2 would be where you have achieved leanfire status,

and stage 3 would be where you have achieved full Financial Independence on your current

lifestyle assuming that it is above the leanfire level. So what do you guys think of this 10 levels

system of tracking our progress to financial Independence? Do any of you use a similar system to track

your progress? If so, what is it and what level, step, or

stage are you guys currently on? Let me know in the comments section below. But that'll do it for me today once again

if you enjoyed this video be sure to subscribe and hit that Bell next to my name so that

you'll be notified of all my future uploads.

I generally upload every single Monday, and

if you have a friend that would be interested in this kind of content be sure to share it

with them and let's really get this information out there and start our own Financial revolution..

How We Retired Early With $540K At 40 In Colorado

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

I started getting

diagnosed with some fairly serious medical

ailments. I just began to realize

that I had been working for a retirement that I

may never enjoy. We just knew we wanted

the freedom to make our own choices with our

time. And that's where

financial independence came in. Then it turned

into how fast can we do this? Let's get it done

as fast as we can. We started to accumulate

real estate in the vein of let's have an

additional source of income besides my job. We accumulated 19 units

over the span of just from 2016 to 2019. I'm Debbie and I'm Chris. We are 43 and live in

Colorado and retired by the age of 40. I never wanted to be a

millionaire. That was never a goal,

even, you know, now in my forties, I just wanted

to have enough money to be able to pay my bills. When I was 21, 22,

somewhere in there, I remember reading The

Millionaire Next Door. It was eye opening to me

because the stories they highlighted in that book

were very similar to what we do. Once it became in

that realm of reality that I could maybe be a

millionaire, then I did become fascinated with

the idea of being a millionaire in both

healthy and unhealthy ways.

Once Debbie left her

job, we're now completely dependent on my job. Honestly, like, I'm sure

there was more than this, but I tell the story

that basically I just stopped going to Subway. Obviously, that's not

the whole case, but that's all it really

felt like. Once we started tracking

our spending a little bit better with budgeting, I

was the guy that was always trying to turn

the knob down on our spending. Chris used to think it

was fun to like try to spend $100 a month on

groceries and just eat what came out of the

pantry.

So we both kind of had

this thought, what if you want to leave your job

someday? That thought easily

turned into how can we use our money to buy us

more time? I was mainly hearing a

lot of stories about rental real estate. Some people were were

building mega empires with rental real estate.

I wasn't looking to do that. I just wanted to

have additional income. And in the in the

process of going from we don't know anything

about being landlords and real estate owners to

let's buy our first property, I scoured the

Internet and spent a lot of time listening to

podcasts, watching YouTube videos, reading

blogs and forums.

And we got this like

eight and a half by eleven vision board type

of thing. So it was just something

that we could write on with chalk that we had

in our kitchen that would remind us of our goals. And, and as I was

writing those goals down, I believe we had like by

the end of 2016, we were going to have two

properties and by the end of 2017 we were going to

have four properties. We were getting

properties that other people didn't want. There was something that

was a bit of an ugly duckling about them. For me, a very difficult

part of this was a lot of elbow grease, fixing up

the ugly things, working on the houses, getting

smoke, smells out, painting everything,

tearing a bunch of flooring out. I'm

spending full days over there. Chris is getting

off work. He's spending nights and

weekends over at these rental properties to get

them ready for tenants and make them nice

places to live.

And as we were doing

that, I'm still saving 50 to 60% of our income

through my paycheck. All the extra money we

weren't spending out of your paycheck was going

toward buying more rental homes. All of the cash

flow we were getting from rentals was going toward

buying more rental homes. We accumulated 19 units

over the span of just from 2016 to 2019.

So it was a pretty

pretty fast and furious four years. We actually ended up

reaching fire at least three years earlier than

we had projected. So gross income from our

rental properties can vary based on vacancy,

capital expenditure, rehab, repairs, those

kinds of things. But it is between 8 to

10000 per month and our net income from our

rental properties is between 4 to 6000 a

month. So the money we live off

of comes purely from our real estate investments. We do have mortgages on

all of our rental properties that we

consider business debt. Our tenants pay those

mortgages for us essentially, and rents

continue to rise as they do so as the mortgage

goes down. Right now, our

investments look like we have about $350,000 in a

combination of traditional IRAs and

Roth IRAs and a brokerage account, $35,000 set

aside in a 529 account for our girls and

another $20,000 in bonds.

The insurance that she

sells for one month a year provides that extra

cushion of safety or comfort, as well as some

other discretionary spending. Our budget now

in FIRE, it looks very similar to what it was

pre FIRE in that none of our categories really

went any different direction except for

travel. We usually have about

$10,000 in our travel budget over the course

of any time, and it's more than we spend. Instead of having a job

where I would work 48 weeks a year and have

four weeks off, I would say now that I work

probably four weeks a year and have 48 weeks

off.

And we found in our lives

that meaning and purpose are important to our

emotional and physical health. And part of that

is around work. We are really enjoying

having this freedom of time to make

connections, to travel and explore. Our

daughters are getting older whether we like it

or not. They'll be graduating

and I'm excited to be a part of of their lives

as they move forward into their next chapters and

have the abundance of time to be able to be in

their lives as much as they will allow us or as

much as as feels comfortable.

I think when we were

searching for financial independence, what we

wanted was freedom and independence from having

to go to a place and do with things someone else

told us to do. And we still want that

and we value that. But I think what we

found through it is a much deeper, fuller,

richer life..

Retirement Tips You Can’t Afford To Miss!

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

we've all heard retirement is not an ending but I think we need to add to the sentence and say it's a gateway to your life's best Adventures wow so dramatic today but like any new chapter in life it's going to you know it this does come with challenges it comes with uncertainties but it also comes with a lot of opportunities you know make no mistake how you prepare today determines the quality of your tomorrow now if you're new here I'm Mark and this is my wife Jody we don't focus on the financial aspects of retirement but rather lifestyle Health relationships and much more so if you like this please hit the Subscribe button and the notification button so you're going to get notified when our new videos come out and gosh it would really be great if you could share this with someone that you care about who's on their retirement Journey too you know we really want you to feel empowered and equipped to face the challenges of retirement with excitement and Clarity and our goal today really is to ignite a proactive approach for you that's that's going to lead you into this next phase of your life you know this is probably actually documented it is one of the biggest changes you're ever going to face in your life and therefore it can be challenging but today we're going to help you find a quick path to success so who do we know that did really well in this uh first part of retirement you know we have we have friends that live in Bronxville New York he had a big corporate job um was you know kind of all over the map all over the world she had her own things that she was doing and I think they've gotten a very successful jump start into their retirement with a couple of key areas that they focused on ahead of time and then they followed through with their plan well one of the things that he's doing is um he is still engaged in some Consulting so he works maybe 10 15 hours a week and you know what's funny Mark we got a lot of push back on the challenge you guys are doing this you're not really retired you're doing that you say people are doing other work they're not really retired I would agree with you so let's just throw the word retirement out yeah that's the thing yeah so what we are is in the next 30 years of our life and charting a new course and for him and for us this is part of what we do we spend 20 hours a week working on this YouTube channel and doing some Consulting and one-on-one coaching but this couple he's doing a little bit of work and she's very active in some nonprofits there's one particular where she's involved with a uh a charity that not a charity U they invest in startup businesses for women she's on the board of this organization so startup businesses started up by women started up by women not just for not big powerful things just women who are U some of them are pretty big and powerful yeah but I mean it's it's really I I didn't mean it that way wow it sounded that way well I didn't I didn't want it to sound like she's on the board of a Fortune 100 company she's a regular person who's helping this organization find women that want to start a business well I I think there's a couple key things and those are the ones that we're going to kind of pull out today some things that when we think of them we know they've done well so so they were they are very successful and we want the same opportunity for you too so let's what what are we going to what's the first tip we call it a tip right well I think um the first thing when you're addressing retirement even before you retire and we've all either started this thought about it done it you have to plan financially so I would say that's number one even though we don't do financial planning right so you need to figure out what your nest egg looks like how much money you have um if you have a pension you know what what that what does that look like coming in what are your obligations you still have a mortgage and a car payment you need to figure all that out and honestly we're big advocates for financial planners because having that outside perspective to give you a voice that's not so tied up emotionally into let's say the stock market which right now poorly um if you're doing all the investment yourself and looking at all you're just going to stress out all the time so having a financial adviser is great and I think just planning financially just at the basic route you know knowing knowing your income whatever that is knowing what you've saved knowing your expenses understanding any diversity of Investments that you have to make sure you're spreading your risk for long-term growth and wrap that all up with engage with a of some kind or even new retirement low we'll put the link below new retirement is a platform that you can buy you can test it for free you can buy it for $120 a year it's phenomenal we use it we have a lot of our clients that use it and it gives you a snapshot of all your finances and there's all sorts of tools in there you can use to uh do what ifs scenario planning really so first thing is planning financially is really really important the second thing that's important and this client we talked about was having a gradual wind down from your career if you have one you know just cold turkey ending it sometimes that's really hard for people and if that's what's going to happen then you certainly want to phase out any work commitments you have you don't want to leave a mess behind right so yeah and I and I think a big part of that phasing out or gradual wind down is starting to set your boundaries right ensuring a balance between what's your work and your personal time so that it's really clear to not only you but to the people that you're still dealing with and and if you're in a case in a situation where you do want to work a little bit you know maybe you can go back to your company and say hey I want to give you 5 hours a week 10 hours a week just something if you work mornings for two hours 5 days a week it gives you reason to get up gives you a little bit of money coming in and it keeps your community alive a little bit longer so you definitely want to see if that's an opportunity with your company absolutely and you know don't be afraid to delegate responsibilities right passing on tasks as you're doing your gradual wind down to people who are either taking your jobs or you know dividing your labor up or whatever it might be I would say that's something good to do and then spend a little bit of time in this gradual wind down reconnecting with your hobbies rediscovering all the passions that you may have put on hold during your career you know what funny we have so many clients that say I don't have any hobbies well because you've been working for so long or you've been involved with other things and if you've never had a you can find one just start you know we're big journalers so writing down what you're thinking about if you spend every morning journaling for five minutes on hobbies and Google what are the most popular hobbies and just start thinking you know what I when I was a kid I used to do that I might be interested in that don't be afraid to explore that and reconnect and try it because it could be that all of a sudden now you're really into I don't know what's a new hobby painting painting or you could clutter your house clean your closet give away all your clothes so so gradual wind down would be the second thing that we really see as a great retirement tip as you get started right the third thing is and I love this one is really taking time to engage in self-reflection you know understanding your identity beyond your work identity and understanding that you're more than your title or your job or your you know even your community at work you're more than that I I want to stay with this for a minute because this is one of the big risks that we all face or the big changes that we all face when we retired because you and I both had identities at work I own my own company I was the CEO and when that ends it's it's really hard to reinvent yourself with a new identity you know my dad struggled with that so much and we did it first and maybe you are too I don't know but you can't just spend the next 30 Years saying I used to do this and I used to to do that really peel back who you are as a human being and that's really your identity and from there you can build something new and I think as you're doing that it's really important to evaluate all your past achievements right it's not like we're saying abandon that and move forward you know really recognize and take pride in your career Journey whatever it was and then move move forward to Envision all the future accompl accomplishments that you could have you know retirement is going to offer you new opportunities you know we get comments a lot that people say Mark stopped interrupting Jody and I just I always respond to that saying we both get so passionate of what we're talking about that I do and I'm really trying hard because I almost just interrupted you I know I'll try hard too CU a l no need to leave that comment I own I I own it and I interrupt jod a lot because I just get so excited about it but you know engaging in this self-reflection you want to you know if you're struggling get get a counselor get a therapist there's nothing wrong with having a therapist and you share your feelings and apprehensions about this phase of life you can't just go through it and not deal with it so it's really important to do that all right what's the fourth thing well for us this is so important establishing a new routine and the reason this is so important and really not to interrupt you just did interrupt I know because I know I'm going to get a comment about that comment about Jody interrupting um it's not just a routine routine it's a new routine oh didn't I say you did but I really think we need to it's not just H they're back on routines this is your new routine well you just keep going with that then and I think it's really important so we have a routine during our career we have a routine if you're a stay-at-home mom or dad you've got a routine but when the other partner comes home or your career ends that routine is shock so you've got to find something that a daily structure you've got to fit in um exercise you've got to fit in some some learning you don't just want to spend 38 hours watching TV every week which is the average number of hours that people over the age of 65 watch TV you don't want to do that enroll in some courses do some workshops online classes volunteer right right and even travel you know and when we say travel you know a lot of you will say well it'd be nice to travel but I can't afford to Trav travel locally go a couple town over overs and explore a coffee shop cou Town overs a couple Towns over what's a couple Town overs a couple towns over is that not a good sent a couple Towns over and you know um just en enjoy and explore like new shops or new restaurants or a new coffee shop or something something local all right the last tip we want to talk about as you're entering retirement is find your fun you know this phase and we struggle here sometimes we always say what are we going to do fun today well we don't have time you have to make room for fun hobby uh joining a club we're pretty good with that we join the YMCA we've got your woman's group I have a men's group we have people with shared interest pickle ball friends um friends we go out to dinner with but you know golf so we want to make sure that we have fun we want to make sure that you have fun and the other part of fun really experimenting try something new or just relaxing and rejuvenating reading a book we never do that yeah we do self-care we do all right so that's important have your fun absolutely and we wanted to make sure we put fun in there because it's not all planning it's not all schedules it's not all routines it's not all our way no this is your time to do it your way and find joy in Simple Pleasures put some structure in it but also have fun cuz this can be a challenging time and it's going to take some getting used to and you want to enter retirement you know this is the beginning of the greatest phase of your life you know try these five tips to begin your retirement with a little hard work but also some fun now if you like this video you're going to like this next one the top five struggles in retirement we talk about loss of community filling your extra time and creating a vision for this phase of life so we'll see you back again soon

Why Some Retirees Succeed and Others Live in Worry – 5 Retirement Truths

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

I want to share one of the most valuable pieces of retirement advice that I've ever heard if you're thinking about your retirement and you're wondering if you're doing the right thing or think that you should be doing something different or if you're just worried about all the things going on right now whether it's the economy or the markets or the value of your accounts be sure to watch this video because I'm going to share the retirement truths that every retiree goes through and it's these things right here we're going to cover today and every retiree goes through it and it they experience this in retirement so it's going to go over this and then also what to expect in retirement and then how to give yourself the best chances of maintaining your lifestyle in retirement as well now the negative of these retirement truths that we're going to look at is that many of them lead to increased uncertainty or worry about your retirement one of our goals though as we're thinking about it is really the opposite of uncertainty or worry in retirement it really should be more about confidence right the next years really all the way up until you pass away wait these are the the magic ears these could be the best years of your life and I know that because there's an actual study a research study uh proving this so let me pull that up really quick and show you the results and I'll link to it below people were asked to score their life satisfaction from zero to ten where 10 is the best possible life and then zero is the worst possible life and this is really just the average score by age and I thought it was encouraging to see that life satisfaction tends to increase as you can see as we get older and then it tends to Trail off as we get older but really the area the the period of time we want to focus on is that this is the magic time and we know this to be true as well because we've helped hundreds of pre-retirees move into retirement with confidence and excitement and these were the people who were coming to us that were feeling somewhat unsure or not 100 confident with their money plan and our firm streamline Financial has been around for 24 years and we've made it through quite a few bad Market periods with our clients and by the way if I haven't met you yet I'm Dave zoller and I own streamline Financial with Tim and Luke and Sean and if you're working with an advisor now that's mainly focused on investments and investment planning but doesn't talk about these key retirement strategies like the tax efficient withdrawal planning and income planning or just tax reduction overall feel free to reach out to us through the website now we don't always have time but I'll get back to you either way so let's get into this first truth in retirement it will be common to have that thought of maybe I should be be making a change or should I be doing something different it'll be normal to feel this way in retirement especially when you see the news or you're listening to friends talk about their finances there's this feeling or this thought of really making us doubt our current plan which causes some people to make more emotional decisions instead of making smart financial decisions and a good way to avoid this is really to avoid this feeling is by having an understanding of your plan which really leads to more confidence with what you're doing and having a plan for both the good times and also the bad Mark of times so that you know that you're prepared for either one of those and I'll give you some ways to achieve this coming up in this video now on to the second thing that comes up in retirement that we just have to be prepared for is we need to expect bear markets right you've most likely lived through a lot of them already and really in retirement though they feel a little bit different usually worse but because of the frequency creating a plan with bear markets in mind and really big Corrections built into the plan is a smart thing to do that way you don't have to worry when they eventually come now if you're not sure how to model out these various what-if scenarios or bad Market scenarios for your plan then you may want to talk to a cfp or check out my favorite retirement income planner below this video you should see a link to it it's one of the best consumer facing planners that I've seen and it doesn't cost thousands of dollars like the ones that we use for our clients the next thing to bring up is for pre-retirees who are close to stopping their wage especially if that's during bad markets they may think should I work a little bit longer maybe just one more year to kind of make it through this this difficult period we actually had a client call us up about five months ago and uh no she was five months into retirement and she said something like it seems like so much bad news is out there and what's going on with the markets I'm wondering if I it would have been better if I should have just kept working so we reviewed her plan and because we built in to her plan this expectation of bad markets everything looked great and and really the only reason to keep working would be if she really enjoyed this sort of work that she was doing and it brought her some some purpose but she didn't so it was great it was great confirmation that she was still on the right track so if this sounds like you take a look at another video I recorded I'm gonna either link on this screen or it'll be below and it gives a few real examples of what working an extra year might look like in a financial plan the next thing to know is that no one really knows what's going to happen next it seems like everybody has a prediction on TV or YouTube or at the dinner table with family or with friends and no one really knows what is definitely going to happen we know this uh in a logical way because you know there's that saying if you put 10 economists in the room together and they come up they need to come up with a conclusion they'll come up with 12 of different answers when they walk out knowing that it's important to prepare your investment plan for that four economic Seasons that we may go through in the future since we don't know which one we're going to go through next so just as as an example you've seen it before the four economic seasons are higher than expected economic growth or lower than expected economic growth and then higher than expected inflation or lower than expected inflation and there's asset classes that can do well in each one of those now again we don't know which way we're headed but having asset classes and each one of those potential Seasons that could be beneficial now that's just my opinion and really it's for all of this talk to your own Financial professionals before doing anything like this now on to the next one which really has more to do with human psychology than investment strategy and then after that I'll share the the really the most helpful piece of advice that I've heard related to retirement planning but if you'd like this so far please click on the the like button and and maybe this video can help somebody else going through the same things that that you're looking forward to so the next truth is in retirement we may have a tendency to compare ourselves to others the grass is always greener on the other side of the fence really throughout life that's we've got that tendency to compare it to others but it can harm us in retirement too if we do a video on this channel that mentions a dollar amount as an example we don't want that to really make you feel better or feel worse about your current situation because you know we help high net worth families at streamline Financial we sometimes mention big numbers but we don't want it to be about the numbers we really want to communicate just the principles and the strategies that can can really be applied to to anybody's finances and there's always going to be people with more than us and then there's always going to be people with less than us and the one who wins is the one who's content and at peace most at peace with their current situation you know that saying if I want to be able to practice being content with a little and I want to be able to practice being content with a lot and and you know healthy competition that's okay but comparing ourselves to someone else because uh you know if it causes us a feel of lack or less than that can hurt our retirement plans because that leads really back to that first point that we talked about in uh in this list of feeling like we should be doing something different for example if we see a guy on the internet and he's investing a certain way or he's deciding he's changing up his entire strategy um because of what's happening with the economy then that may cause us to feel like we should be doing something different and then start to increase the emotional level of uh of our decision making instead of staying to strictly logical or financial levels but again it's a normal feeling to feel that worry or fear or anxiety um with what's happening during during current periods but one of the most helpful pieces of advice that I've heard that we can apply to retirement planning is really the difference between those two words fear and anxiety knowing the difference between those two is actually very very helpful as we're planning retirement and talking about money that is if we want to feel better about what we're doing right now when we think about fear and anxiety we might think of them as being the same thing but actually they're completely different things and let me just pull up these two definitions if I can really quickly fear is a caution over a real and present danger and then anxiety is a worry over an imagined future danger now fear if we've got something right in front of us then it's obviously a very helpful tool for us as humans anxiety though is not always a helpful tool as as we're trying to process things partly because these anxieties there's nothing we can do to control or influence them you may have seen this drawing from Carl Richards before about things that matter and then things I can control here's a place to focus and then another way to look at it is we actually sent this to clients not too long ago on a video of what you can't control and what you can control so we can't control the markets and inflation and what they're doing with interest rates or what's happening in the news or the world or tax laws or the elections but a lot of these things actually do relate to things that we can control for instance you know markets are inflation or interest rates your portfolio allocation you can control that you can control when to pay taxes when it's related to in investing you know as we're talking about Roth conversions or the the costs the tax cost tax drag on some of the portfolio and not to get too nerdy about these things but two of the biggest things that we've seen is this idea of not controlling the news but what we can control is news consumption we've seen a big shift with uh some people who instead of someone who wants to consume the news they switch from TV news to reading news where you have a little bit more control of what's coming at you versus TV is just the next thing is coming at you if you know what I mean I don't know if that's if I if I'm explaining that the right way but back to the this video all the things that we mentioned before earlier here um a lot of these can be anxiety-inducing things as well right the severity of a bear Market or not being able to predict what's going to happen next in the world or comparing ourselves and doubting our plan or thinking that we don't have as much as as we wish we had when it comes to to money or the you know what if this happens and what if this happens how is that going to impact my plan and that can lead that sort of thinking can lead to paralysis and really no action being taken but what if you had a plan that was built in to show those different what-if scenarios so instead of the unknown future danger you're able to get more concrete scenarios in the plan as a result that's what I would recommend once you get get it out in the open then it becomes a lot less scary we both know that so either find a great certified financial planner who can show you that and show you the what-if scenarios or check out the the DIY planner or a different planner that helps you put in those what-if scenarios as well so it becomes less scary so don't forget anxiety is it can be the thief of Dreams it takes you away from enjoying the the present moment and it stops you from even taking the right action to make things better in the future because it really just makes you only focused on on the negative as you're you're moving through life that video that I mentioned earlier is called why delaying retirement might not be a good idea if you're pre-retirement and you're thinking you want to work a little bit longer because of what's going on take a look at that one coming up next or below and then I'll see you in the next video take care foreign [Music]

What Do You Do With Yourself After Retirement? – Dr. Devi Shetty with Sadhguru

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Devi Shetty: Sadhguru, I am constantly torn between my senior colleagues, who are extremely skilled surgeons. Sadhguru, the… on the heart there are some procedures, which are done by very few people on this planet. I’ll give an example – I do an operation called pulmonary endarterectomy that’s the blood clots from the leg goes to the lung arteries and it clogs up all the arteries. So twenty… twenty-five years ago there was no cure for this. And once you are diagnosed, you are destined to die within a year. Today people who are on home oxygen for two years, three years you do the operation they can go back to skydiving or they can go to scuba diving. That’s the transformative effect but there are only fifty surgeons less than fifty surgeons in this world who can operate. And like this we have some of my colleagues who are extremely gifted surgeons. They are in their fifties now. And some of them are constantly talking about retirement.

Especially one surgeon he is a extremely gifted surgeon who can fix any damaged valve. He is single, he has no other commitments every other day he talks about going to Banaras or somewhere and retire and I keep telling him that God didn’t create him to retire and meditate. He has to be fixing all these problems So he gives me extension every six months Guruji. So at the end of six months the usual rigmarole starts, he talks about retirement and everybody is depressed in the hospital. So how do you deal with this kind of people? Sadhguru: You must you must give him a one year sabbatical with me Yes, because the need or the idea of retirement enters anybody’s mind because of the monotony of what they’re doing, whatever it may be.

Somebody else may think it's a great thing but in your experience somewhere it's becoming monotonous or stagnant. Stagnation is one thing that human intelligence and human system cannot take. And most of the ailments are because of stagnation stagnation of life. They may be… they may be getting their you know once in three years promotion. They may be making little more money. All these things may be happening but somewhere experientially there’s a stagnation, which could be a major cause for many of the complex ailments that people manufacture within their systems.

The more complex they get you try to create more talented surgeons. I am saying we are manufacturing the problems, we are trying to manufacture a solution. I think as we offer solutions people who have adl… already gotten into problems, they need solutions. But it's very important that we teach people how not to create these problems, so that instead of fifty, you have to produce five thousand expert surgeons to attend to all these people who are on self-help to illness. So I would say a surgeon who is who has a certain competence and who has worked through his life, if he wants to explore something of his own nature, that will be the greatest thing to do because he is not a man without commitment nor competence.

When competence and commitment is there, you should not run him through the rig ram role (rigmarole?) and destroy that possibility. It’s important that he explores something of his own nature, which will make him We don't know what he’ll come up with. You cannot even estimate what he may come up with. I think a sabbatical is good. He may come up with something that you have not thought possible. Devi Shetty: I will… I will convey your message Sadhguru. I am sure he is watching this program.

Read More

Retirement Financial Advice: Money Lessons You Need to Know in Retirement

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

once your earning years are over and you've built Your Nest Egg for retirement you need to be smart about so many decisions now we're not financial planners and we make that very clear with everyone but we are retired and we do spend time making sure we're doing the right thing financially with our own money because oh bad financial habits and lack of knowledge can actually ruin your we have we have a couple they're good friends and he felt like he knew what to do with the marketplace with his Investments and he clearly didn't because he had his money in stocks when it when they went down and he pulled it out and put it into cash when it went up so for eight years he was on the wrong side of every single one of the stock market moves and because of that he lost a significant amount of his retirement assets and that's really difficult and today we find that they're struggling many of their dreams have vanished and they both actually had to go back to work now there's nothing wrong with work but it's just not what they had planned so we can't emphasize enough right out of the shoot having a financial planner is so important because it gives you a plan it gives you a vision it gives you an idea but it also does this which I think is most important it takes the emotion out of the marketplace which can get the best of you think you know what's going to happen at a new presidential election and frankly you don't that's right so let the experts help you with that because we don't want to have what happened to them happen to you today we want to share some practical ideas that may maintain or even improve your financial situation and again the number one lesson today is don't manage your money without a financial planner and we don't mean a stock broker what we mean is someone who has a fiduciary responsibility to make recommendations that are are really good for you not good for them and they talk to you about the strategies and you might say well sure they do but they also talk to you about withdrawal strategies right how much should you be withdrawing each year in order to preserve your nest day how much do you need each month and then they pull it from the smartest place it needs to come from using tools like tax loss harvesting you can't just take money out of a stock because you want to because you're going to have capital gains right right and you know we're not a big fan of multiple planners but we'll leave that part up to you so the first one is make sure you get a financial planner somebody you're comfortable with the second is keep your emergency fund intact kind of no matter what you need to have emergency savings that doesn't disappear when you retire it's more important than ever to have accessible cash set aside for any type of emergency so two three four months of expenses in a cash account that way your financial planner can invest the rest of your money and always always be thinking about you're going to need more money in 60 days so what can they put you into short term so you want to have this cash account so you can cover any kind of emergency expenses or just if you want to leave stuff in the market a little bit longer you've got some cash or even if you have any big purchases that are coming down the pipe that's true making sure your financial planner knows that you're ready for that so the second thing is the emergency fund now here's another um here's another way that you can get into trouble or you're also a way to dig yourself out of trouble you want to take a look at all your luxuries and make sure that they haven't become a burden because frankly that happened to us we both had jobs we were both working gosh 15 years ago we bought our first boat and we bought four boats over the next 15 years but we could afford it because we both were working we both had money and it was our floating vacation home so to speak I I call the last one that we had a lifestyle about because we went away on that one a lot it was a little bit larger but once we were tired all of a sudden it was like well we don't really want to go out on it the weather isn't good you know we'd rather stay home we'd rather be with for the price of diesel or the price of gas you know the price of storage the price of hauling the price you know all of those things have to be factored in when you have a fixed income yeah and we didn't have the same earning capacity to kind of keep up with the luxury so we stopped using it and then it became a burden like why aren't we using it and it was a year ago now that we decided to sell it and it's sold within a month because we kept really good care of it but the thing is if you have luxuries it's really important to take a look at them and say that's something we're really getting a lot of satisfaction of because it's going to cost you money well there are also luxuries that you have and then there's luxuries you provide for others right so we have six children and we were providing cell phones homeowners insurance auto insurance airline tickets for them and their significant others are partners and you know that was all fine when we were dual income but as they aged and as we aged and as we came into a fixed income place we needed to start peeling some away and giving those responsibilities back to them and they can afford it they all have great jobs and if they're ever stopped but it was a luxury it was to be able to do that for him but but frankly it also gave us a lot of satisfaction a lot of fulfillment to be able to help them right so it was hard for us to Pivot to in our mind take these things away from the kids but they you know at some point they've got to be to stand on their own two feet so and we needed to reduce the support so we sold the boat we paid off two car loans we came to an agreement with the kids and slowly weaning them off of some of these things we've always paid for you know because they they can't afford it and you know they they they're fine with it right they even they say it's kind of silly that you're paying my cell phone bills so it's it's another cord to cut that um you know it's hard to do but we want to encourage you to do it yeah so that was the third one the fourth one is you know really trying to figure out how to live a little below your means you know and that's new for us for our entire career as our income went up our living style and our cost of living and everything we did went up with it you know hard work learning and growing you know we were climbing the corporate ladder Mark was building his business you know it was easy to have your lifestyle kind of follow you yeah and you know we both come from humble beginnings and we improved our lifestyle as we went up but then then it's sort of when when you retire you have to think okay well my income's not going to keep going up as a matter of fact it's going to go down so how do we want to live what are some things we can do to live within our means and even underneath our means so and there were a couple things we had to agree to right so you know I call it shopping for sport right so there's there's no more you're better at that than pickleball kind of just opening up and saying oh you know look what just came into my feed I'll take a look at those earrings or that bracelet or those dresses or those sunglasses I think about it I kind of have a little bit of a sunglass addiction so so you know there was you know we agreed that we would do no more shopping for sport yeah it was one of Instagram Amazon it's so easy to spend money today and you get hooked on this new game you don't even leave your house you don't even leave your house you know keeping up with the Joneses that's not necessary anymore right you know who are the Joneses anyway today it's other retirees we're not taking on any more debt we've paid down most of our debt you know again we have a financial planner and you know we have a more modest wardrobe I mean our fancy or fanciest clothes are for our YouTube channel right and we're eating out less we made the agreement that for health and economic reasons we would eat out less so leave living below your means is something you can control and it's something that you can put some time and intention into so another really important thing to get to know is everything about social security and we we don't know that much about it so our financial planner and our accountant has said you don't need to take it yet and that's kind of all we're thinking about at this point they'll let us know when it makes sense and when it makes sense it'll make sense but you have to really understand or have someone coaching you on what's important because everyone's financial situation is different yeah and I really believe the more you know about it the better off you'll be even if you do your own investigation you know Social Security was not meant to be your primary source of income as you age in America it was meant to be a supplemental income so you have to understand the amounts you can get at what future ages and can you still work and does your state tax it or not you know there's a lot of rules around Social Security and my recommendation would be just get to know your rules in your state around your age just for the knowledge I don't know but I think there's a certain amount of uh you can't earn a certain amount of money and still get Social Security I don't really know but you have to know that's I guess that's the point you really need to know everything about social security check with your account and your financial plan right here's a big one for us and it should be for you too I think you know money will never buy you happiness and we've heard that like our whole lives and so we actually did a little bit of research and you know what really defines happiness for us and we came across this quote and part of it is from Warren Buffett but it says you know we want to do what we want when we want with whom we want for as long as we want and that to us will Define our happiness you know now some of what you do will require money but it's not all about buying stuff and things you know most of what we do for happiness now is experiences I I would think that for us and tell me if you agree but the something we just spent money on is giving us more happiness now for a very low value than anything else I remember paying forever you know what it is your pickleball racket pickleball so we joined the YMCA uh for like eighty dollars a month for the family we bought a pickleball racket for 100 bucks and six balls for eighteen dollars and we're getting like five or six hours of use out of that each week yeah that's happiness that really is making us happy it's not a new car it's not a new set of golf clubs right it's not what we're used to thinking that was um would create happiness and we're also looking at vacations differently right now that we have the full seven days to ourselves many vacations to visit friends or family you know they become Tuesday Wednesday Thursday versus the high traffic weekend Friday Saturday Sunday so many vacations Beach days lunch dates you know we just renting a boat for a day we're doing that with company comes we're renting pontoon boats now for the day to take companies out it's three hundred dollars for a day which in one respect sounds like a lot but it's a lot cheaper than owning a boat right that's true so we still get out on the water now look you clearly need money in retirement we all can agree on that but how much do you need and how much is enough you've got to figure out how much you have how much you can pull out each month and how long it's going to last those are key questions you need to work through with your planner and your account yep and paying attention to some of these things that we just shared will help guide you and keep you out of trouble now we hope you enjoyed this video and if you did you're going to like this next one called the truth about early retirement what they don't tell you it's one of our most popular videos and you know we're not getting any younger so why steal these fabulous years from ourselves our family and our friends watch this one next

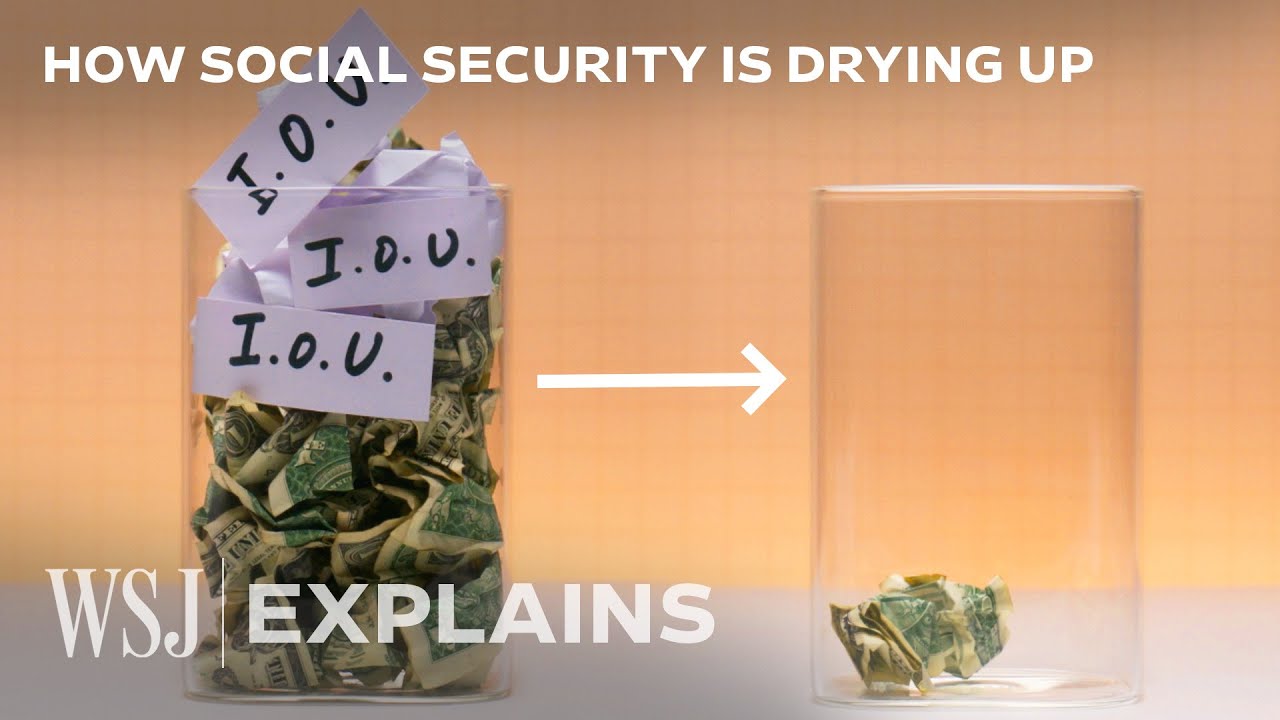

How 2024’s Record Retirement Numbers Could Spark a Recession | WSJ

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

– [Narrator] You're looking at

a chart of the US population, and these are the baby boomers. This year, a record number of them will reach

traditional retirement age. By 2030, they'll all be 65 or older. This is creating a fiscal problem because fewer taxable

workers means less money for social security. – If Congress does nothing,

we're gonna hit a major crisis.

– [Narrator] Here's how

this demographic shift threatens the future of one of the country's most

important government programs and what can be done to fix it. Baby boomers or those born between 1946 and 1964 have been propping

up the US economy for decades. – Their mere numbers

contributed for a long time to rapid economic growth and because every worker

contributed social security that made social security

look very healthy. – [Narrator] But as boomers

started exiting the workforce in 2008, the number of

retirees grew rapidly. – Not only do you have more

retirees collecting benefits for more years, you

have fewer young people entering the workforce

because birth rates were lower for their parents' generation, and that creates a squeeze

on both directions.

Higher expenses from all

those retirees living longer, lower payroll tax revenue from fewer people entering the labor force because of those declining birth rates. – [Narrator] This puts a lot

of pressure on social security and without policy change, projections show the trust

funds will be depleted in 2034. – There's a misconception out there that when the social security

trust fund is exhausted, the system is somehow

bankrupt and there's no money. Social security is an integral part of the federal government, and as long as the federal

government is not bankrupt, social security is not bankrupt. – What's really happening is

the program is running out of treasury bonds, which are basically IOUs

from the government. For many years, social security

was taking in more money than it needed to pay out in

benefits, so it lent money to the government to

use for other programs, and it got IOUs in return. – Around 10 years ago though,

that situation flipped around.

For the last decade, we've been

paying out more in benefits than we've been collecting

in social security revenue. – [Narrator] But because the program had so many IOUs stashed

away from previous years, it's been able to keep

paying benefits in full by cashing in on those IOUs. – Right now, there's

roughly $3 trillion in IOUs, but each year that $3 trillion stash gets a little bit smaller. By the year 2034, all of the

IOUs will have been cashed in. – That means retirees would see overnight about a 25% benefit cut. – [Narrator] This number will

likely increase as the number of workers per retiree continues to fall. – Simply because we're not about to go bankrupt doesn't

mean there's no problem.

There very much is a problem. – [Narrator] Studies

show that the majority of Americans rely on these

monthly benefits checks for retirement income. According to census bureau

data, about 50% of people between 55 and 66 years old

have no retirement savings. – Can you imagine right now if you had to take a 25% reduction

in your take home pay, you still have to pay rent. You gotta buy groceries,

you gotta pay utilities. – It's especially important for those who don't have college degrees, people on the lower end

of the income spectrum. – [Narrator] Fichtner says, when retirees have less retirement income, they also generally spend less money. – That means less economic activity. That means less employment because employers have to lay off people 'cause no longer is that money coming in. It's a ripple effect that could be basically a

senior induced recession. – But social security is only

meant to replace a percentage of a worker's pre-retirement income based on lifetime earnings. So as much as 78% for very

low earners to about 42% for medium earners and

28% for maximum earners. – This is three legged stool

we talk about all the time.

It's supposed to be social

security is one leg, your employer provided pension is a second leg and your

personal savings a third. Well, social security

is financial challenges. We don't have pensions really anymore. About 10% of the population has pensions and then it's hard to save on your own when you've gotta pay off student loans and housing costs are so high. – [Narrator] About half of Americans do have retirement accounts

like 401Ks and IRAs, but those are all subject to market risk. – I hear a lot, well,

those are 65 year olds.

Why do I have to worry