Tag: how to retire at 30

10 Levels of Financial Independence And Early Retirement | How to Retire Early

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Long-term financial goals can sometimes seem

so big that they feel almost unattainable especially when we’re just getting started

on our road to financial independence. I and many others like me in the financially

independent, retired early community have found it helpful to break down the goal of

becoming financially independent into smaller and more manageable levels of financial independence. Not only because it makes it easier for us

to track our progress, which in turns helps us to stay motivated throughout the process,

but also because it helps us get over that initial hurdle of starting to chip away at

this mountain of a task. In today’s video, I’m going to take you

through what I consider to be the 10 levels of financial independence as well as give

an example on how to go from the first level to the top level in your lifetime. Hey everyone Daniel here and welcome to Next

Level Life a channel where you can learn about Investing, debt, retirement, and many other

general financial education videos because the school's aren't going to do it for us.

So if any of those topics sound interesting

to you or if you want to learn how to better handle your money and have more financial

freedom be sure to hit that subscribe button and the bell next to my name to be notified

every time I upload a video. And if you want to further support the growth

of this channel you can check out some of the links I’ve left down in the description

below which includes a 30-day free trial of Audible and 2 free audiobooks of your choice

as well as a list of some books on money I’d recommend checking out, or you can share this

video with a friend, and leave a comment below letting me know what topics you’d like me

to cover in future videos.

Now obviously these ideas of the levels of

financial independence are not solely my own nor are they very new as there are many articles

and blog posts that have covered this topic already and have done so for many years. So consider this more of a summary of many

of the ideas expressed in those articles and if you want to learn more about the topic

feel free to check out some of the articles for yourself. I’ve left some links in the description. With that out of the way, let’s get started. Okay so real quick the 10 levels of financial

Independence are Level 0 Financial dependence, level 1 Financial solvency, level 2 Financial

stability, level 3 debt Freedom, level four coasting Financial Independence (also sometimes

known as freedom from employer), level 5 Financial Security, level six Financial flexibility,

level 7 Financial independence, level eight Financial Freedom, and finally level 9 Financial

abundance. The levels are usually defined as something

like the following: Level 0 – Financial dependency is when your

debt payments and other living expenses are greater than your own income.

This means that you are in one way or another

dependent on someone or something else to help you pay for your bills or if you happen

to be a kid and don't actually have any bills you need someone else, usually your parents,

to pay to put food on the table and keep the lights on and have a roof over your head. This is the level that all of us start out

on and it is referred to as level 0 because as a financial dependent you obviously have

no Financial Independence. Level 1 – Financial solvency is when you are

current on all your debt payments and you can meet your financial commitments and your

other living expenses without any outside help. Level 2 – Financial stability is usually defined

as when you have built some sort of emergency fund in addition to being financially solvent. Level 3 – Is again debt freedom and it's defined

differently depending on who you ask. For some, it is being completely debt-free,

mortgage and everything.

For others, it's being just free of the high-interest

debts like credit cards but you still might have a mortgage or other debts like student

loans. And for some others, it is paying off all

of your debts except for the mortgage but your credit cards and student loans or car

loans all that stuff is all paid off. Level 4 – Coasting Financial Independence

also sometimes known as freedom from the employer, Barista Financial Independence, or Agency

in blogs and other mediums. I personally like the idea of it being coasting

Financial Independence so that's what I'm going to be using in this video but know that

some people refer to it by one of those other titles but the idea is the same. You have reached the level of coasting Financial

Independence when you could, if you wanted to, step down from a job that may be higher-paying

but may also be either less satisfying or more stressful or both into a new job that

is lower paying but more enjoyable or less stressful or both.

This is because in the early years of your

career or just thought most recent years you have managed to save a very decent sum of

money that would be able to provide for the later years of your retirement after it has

grown even if you don't put much more in. Therefore all you need to do is make enough

money to get you to age 60 or 65 or 70 or whatever your numbers work out to be when

that amount of money you've already invested will be able to fund your lifestyle because

it's been given enough time to grow. So in a sense, you've worked really really

hard and been very frugal in the first few years so that you can coast into your retirement. I have gone into more detail on the various

types of financial Independence in a previous video which I'll leave Linked In the description

if you're interested in learning more.

Level 5 – Financial Security is effectively

when your cash flow from wealth such as you are investments has grown to large enough

that it can provide for your annual basic survival expenses. Now I say survival expenses because I do differentiate

that from living expenses survival expenses are just the basic things you need to survive

Food, Water, Shelter, some form of transportation, clothing and probably insurance. This does not include things like Netflix

subscriptions or cable bills or things like that it is purely survival expenses. So this may not be exactly the ideal spot

to retire and I certainly wouldn't want to retire at this point but it is an important

level to keep in mind because it does give you… well security. If you were to get fired today and you were

on level 5 you would be okay you could survive until you found another job. This is essentially the first level that really

gives you I guess that piece of mind even if the lifestyle should you have chosen to

live it may not be the most lavish.

Level 6 – Financial flexibility is similar

to Financial Security just one step up. It is when you have the ability to live off

of your current cash flow from your wealth assuming that you have a flexible spending

plan that adjusts for up and downs in the market. So if the markets up 20% one year you're able

to spend a little bit more but if the market is down 20% the next year then you don't spend

quite as much. I’ve seen it defined many different ways

so it could vary depending on who you ask, but the one that I personally like the most

is that it is roughly half of your full financial independence goal, or roughly about 12.5x

your current annual expenses if you follow the 4% rule to get an idea of how much money

you need to retire like I’ve explained in previous videos.

So it isn't quite Financial Independence yet

but it's close. Level 7 – Is financial Independence and it's

usually based on the 4% rule which I have covered in a previous video. You can follow the 4% rule when you have saved

roughly 25x your annual expenses. The vast majority of the time this will be

enough money to allow you to maintain your current lifestyle in retirement and as a result,

you can be considered financially independent. And some articles end it right there but I

think there are a couple of levels that are a bit higher than that that are worth considering

even if some of us may decide to not ever try to achieve them because being at level

7 allows them to do what they wanted all along. So let's talk about those other levels. Level 8 – Is Financial Freedom which I've

often seen defined as the cash flow from your Investments is greater than financial Independence

and a few more life goals.

Life goals, of course, will differ for everybody

but this is could be something like taking a trip or two overseas or moving to a new

place you've always wanted to live but haven't had quite enough money to live there up till

now or whatever the case may be for you like I said it's different for everybody. Level 9 – Is financial abundance and this

is quite simply just that the cash flow from your Investments is more than you will ever

need.

You could spend it if you really wanted to

but it would actually take some effort. And the stuff from level 8 doesn't really

cut into it much at all. So you could up those goals even more and

still have more cash flow left over at the end of the year. This also probably has a slightly different

definition for each person depending on who you ask, but I like to think of it as roughly

3x your financial freedom number because this would allow you to experience a horrible bear

market where your investments go down by 50% and still has 1.5x the amount that you would

need to maintain the lifestyle you lead when you reach level 8.

To me, that means that it is likely more than

you will ever need, but again that one is strictly my own opinion on the matter. So those are the 10 levels of financial Independence,

now let's walk through a hypothetical example of how someone could go from Level 0 to being

financially independent in a single lifetime. John and Jane are recently married couple

each making $20 an hour at age 23 or $83,200 a year between them assuming no overtime. They manage this because they are not only

good hard-working people but got great grades in school and we're selective about the job

that they decided to pursue. Obviously just like everyone else they would

have started off as Financial dependents and as they were going through college they would

have been building up student loans that they would not have had the money to pay off (assuming

of course that they didn't earn enough money while in school to keep up with the rising

debt).

In all they have credit card debt, two car

payments and the student loans which have balances of $5,000, $35,000, and $60,000 respectively,

but since they got their jobs they are no longer financially dependent and their incomes

have allowed them to become current on all their debt payments without the help of others. In addition to the regular monthly debt payments,

their annual expenses are $48,000 a year. So they are currently in level one Financial

solvency and trying to figure out a way to move to level 2 Financial stability. In order to do that they need to figure out

a way to build up an emergency fund.

Now if they're following the 10 levels system

to a T then they would look to build a 3 to 6-month emergency fund of their survival expenses. However, this is not the only way to approach

it say if you were to follow Dave Ramsey 7 baby steps you would start off with just a

$1,000 starter emergency fund and then get right onto attacking your debts. And other Financial systems and plans may

have you approached it an entirely different way.

Either way is perfectly fine because the 10

levels system is not meant to be a financial formula per say it's more there to give us

some sort of guidepost so that we can better track our progress towards achieving Financial

Independence. But for the purposes of this video, I am going

to assume that they follow the 10 levels in order so we are going to be building up a

full emergency fund. In order to find how much of an emergency

fund they will need we will need to know how much money they need to survive not necessarily

on their current level of expenses while they have jobs but purely on Survival expenses

which are basically your four walls of your financial house or in other words food shelter

including utilities Basic clothing and some form of transportation as well as the insurances

that are related to that assuming there are any.

In this case, I'm going to assume that their

survival expenses are right around $3,000 a month. Which means that in order to get a 3-month

emergency fund they would need $9,000 in order to get a six-month emergency fund they would

need to save $18,000. Both John and Jane feel that their jobs are

pretty darn secure and the market is doing fairly well so it's not likely at least in

the near-term that they would get laid off because the company has to downsize so they

decide together that they are comfortable with having just a 3-month emergency fund

of $9,000. So with $83,200 a year in income, $48,000

a year and expenses, plus minimum monthly payments of $100 on the credit card which

is 2% of the balance, $550.78 on the car loans, and $621.83 on the student loans they will

have approximately $1,660.72 a month left over to start building their emergency fund.

However, both John and Jane have been looking

into their finances and researching a lot lately and they become fired up at the possibility

of becoming financially independent while they're still young. So they want to see if there's a way that

they can speed this whole process up. And as it turns out thankfully there are many. After taking a look at the options they decide

that they're going to work as much overtime as they possibly can (for the sake of Simplicity

I'm going to assume that they manage to work on average 5 hours per week of overtime which

will increase their monthly income by about $1,300 a month, meaning that instead of $1,660

a month they will have $2,960 a month left over) and they're going to sell both of their

cars and buy some nice used cars with cash to help knock down some of that initial debt. After putting out a couple of ads online they

managed to find buyers for each of their cars that is willing to give them $15,000.

So they take that $30,000 and use $5,000 of

it to pay off the credit card balance and another $10,000 to buy a couple of used cars

from someone that they know takes good care of their Vehicles whether that be a family

friend or just a mechanic that they Trust. The remaining $15,000 is thrown at their car

loans. This means that the credit card loan is fully

paid off and therefore the hundred-dollar minimum payment is no longer needed. So John and Jane start throwing $3,060 per

month into their emergency fund and get it fully funded in 3 months with a little bit

left over at the end of the third month to throw out their car loan. Over the course of those first three months,

they managed to bring the car loans balances down to $18,423 thanks in large part to the

$15,000 that they threw at it in the first month after selling the cars and also making

the minimum payments in the first three months. Now that their emergency fund is fully funded

however they're able to throw that $3,060 a month in addition to the $550 a month minimum

payment at the car loan and get it paid off in 6 months flat.

So a mere nine months into their Journey John

and Jane not only have a fully funded emergency fund but they also have paid off both of their

car loans. Now there are just the student loans to tackle. And thanks to the fact that they've been making

minimum payments on them for 9 months and the fact that they had a little over $3,000

at the end of the ninth month after paying off their car loans their student loans now

have a balance of $53,263. John and Jane follow the same pattern that

they did with the car loans throwing the $3,600+ which is what they now have left over at the

end of every month because they no longer had a $550 car payment to make and they managed

to get their student loans paid off in full in 13 months. So John and Jane have managed to become debt

free and have a fully funded emergency fund in 22 months.

They have now reached level three and because

of that they now have over $4,200 a month left over to start investing. This brings us to level four coasting Financial

Independence. Let's assume that John and Jane want to retire

by the age of 65. That means that whatever they put in now needs

to be enough to grow to a point where it can support their lifestyle in retirement by the

time they're 65. If we assume a rate of return on an average

in the market of about 10% before inflation and an inflation rate of about 3% per year

on average then we can get a rough estimate of how much John and Jane need to put away

in order to achieve a state of coasting Financial Independence. In this case, since they're 24 about to be

25 they will have somewhere in the neighborhood of 39 or 40 years to let the money grow before

needing to take any of it out. If their expenses were $48,000 a year at age

23 then 42 years later if we assume a 3% rate of inflation they would need a tad bit over

$166,000 each year to live on.

Again assuming we follow the 4% rule to figure

out how much they need once they fully retire to be financially independent that means that

they would have to have at least $4.15 million invested in the market by the time they turn

65. In their case, they would need about $110,000

saved up give or take in order to achieve coasting Financial Independence and because

they're able to save about $4,233 a month now that they’re debt free, they’re able

to hit that goal in 2 years flat.

Meaning that in theory, they would be able

to step down from their jobs to a more rewarding less stressful but probably lower-paying job

just 3 years and 10 months into their financial Journey. That is incredible! But like I said coasting Financial Independence

wasn't their end goal. They wanted to be fully Financial Independent

so they keep working and investing for now. The next level is level 5 Financial Security

which is achieved when your cash flow from your Investments is greater than your annual

survival expenses which remember is $3,000 a month or $36,000 a year in John and James

case. Because they are debt-free, are making good

money at their jobs, and being intentional with their finances they Achieve Financial

Security in a little over 4 years with over $367,000 in their portfolio.

It is been a mere 87 months or 7 years and

3 months since they began their financial Journey. John and Jane are 30 years old and they are

able to get by on their Investments alone. In theory, they could retire now, it wouldn't

be the most glamorous retirement and it wasn't their goal but it is an option they have. They don't have to worry about losing their

jobs anymore because even if both of them lost their jobs today they would be able to

make it long enough to either find a new job or some other source of income. This is really the first level where you start

to get that piece of mind when it comes to money at least in my opinion. Next is financial flexibility which as I mentioned

earlier in the video has many definitions depending on who you ask but for the purposes

of this video, I'm assuming that it is roughly 12.5x your current annual expenses which for

John and Jane would be roughly $600,000 or about $855,000 if you account for inflation. This means that they would Achieve Financial

flexibility 9 years and 8 months into their Journey not accounting for inflation or about

11 years and 9 months if we do account for inflation.

John and Jane continue investing through all

the highs and lows of the markets until they reach Financial Independence exactly 14 years

into their financial Journey assuming we don't account for inflation or 18 years and 3 months

if we do. So you might be wondering why did I split

up the accounting for inflation time frames and the not accounting for inflation time

frames should we always be accounting for inflation? Well technically yes but the reason I split

them up is because in my experience taking this journey myself as well as seeing others

take it, this journey changes how you view a lot of things and more often than not those

changes lead to you valuing things such as freedom of mobility and location and freedom

of time to be able to spend with the people you love more and valuing more material things

that cost possibly a lot of money less and less. That's not to say that everybody becomes minimalist

going through this journey, I'm not saying that at all but I have seen a lot of people

who have gone through this journey become closer to minimalist than they were when they

started the journey as they find out more and more things that they used to buy just

don’t provide enough value or happiness for them to be worth the purchase.

They find better uses for their money and

time and as a result, they generally tend to spend less. Which means that even though inflation is

technically increasing your expenses by making every dollar less and less valuable over time,

if you're also decreasing your expenses because what you value is changing it may even out

or in some cases, you may even see your regular expenses going down year-over-year as you

continue through this journey. So that's why I split them up. And, before I go, I do want to mention that

based on what I've seen on various articles and forums some people really like to have

even more goals to chase as they go through this journey than what I've laid out today

in this video so if that's something that would help you feel free to break down these

levels even further then I have today this is obviously just the list that I used and

what worked for me, but you could take it even further.

For example, Debt Freedom could be broken

down into three separate stages: One where you are free from all high-interest debt,

a second where you are free from all debts except for the house (if you have one), and

a third where you are totally debt-free. You could tackle the coasting Financial Independence

level in a similar way breaking it down into two stages: One where are you have invested

enough to survive in retirement and a second where you have invested enough in order to

maintain your current lifestyle, adjusting for inflation of course, in retirement.

And the financial independence level could

also be broken down into three stages: Stage one would be where you are at a survivable

level of financial Independence, stage 2 would be where you have achieved leanfire status,

and stage 3 would be where you have achieved full Financial Independence on your current

lifestyle assuming that it is above the leanfire level. So what do you guys think of this 10 levels

system of tracking our progress to financial Independence? Do any of you use a similar system to track

your progress? If so, what is it and what level, step, or

stage are you guys currently on? Let me know in the comments section below. But that'll do it for me today once again

if you enjoyed this video be sure to subscribe and hit that Bell next to my name so that

you'll be notified of all my future uploads.

I generally upload every single Monday, and

if you have a friend that would be interested in this kind of content be sure to share it

with them and let's really get this information out there and start our own Financial revolution..

How To Retire At 30 Living Off Investments

Jason 0 Comments Retire Wealthy Retirement Planning

in order to live off of

your investments completely. And I know that the title of this video may sound crazy about retiring by 30, and there are a lot of people

out there selling a pipe dream of you can retire by 30

as long as you invest in this course, or go buy real estate and while that may work for some people I'm not here to sell you guys a course or to pitch you on any

kind of product like that. What we're going to

simply talk about here is how much money you need to have invested in order to live off of your investments and essentially not have

to work to earn your money. And believe it or not, there's

actually countless people out there who have in fact

retired as early as 30 years old, by following this exact strategy

that I'm going to outline. So if this idea of retiring early and not having to work for your money is something that interests you. What I want to ask you

guys to do is go ahead and drop a like on this

video just show your support.

I really do appreciate

that as it helps out with the algorithm and allows this video to get shared with more people. But what we're going to look

at in particular in this video is something called the 4% rule, and that essentially

shows you just how much money you need to have set aside, in order to live

off of your investments. Now you can in fact live off of different types of investments like real estate or the stock market for

example or a business that's providing income for you. But what we're going to use in this video as an example is a passive

stock market investment, and we'll show you exactly

how much money you need to have invested in order

to live off of that income. So the goal here with this

strategy is to simply invest your money and have a large

amount of money invested and then you would

essentially be living off of the interest income or

the growth of that money without touching the principle.

And as I'm sure you guys can imagine if you're not touching the principle or your initial investment, then your money could

foreseeably last forever. Now, the sooner you're able to retire is all based on how much

money you're able to save up and how little money you are

spending each and every month, and there's actually a

whole movement of people that are following this

exact strategy, and it's something out there called FIRE, and FIRE stands for financial

independence retire early. And there's a lot of

people who are doing blogs and videos and all kinds of

stuff about this concept, and there are countless

examples out there, of people who have retired

as early as 30 or even less. By following these strategies. Alright guys so there's

basically three steps you have to follow in order to do this, and as I'm sure you can imagine, step number one is to be frugal or to spend as little money as possible, because ultimately what

you're looking to do is save and invest enough

money that the interest or the dividends, or

whatever the growth is pays for your monthly living expenses.

And as I'm sure you guys can guess if your monthly expenses

are $6,000 versus $3,000, you're going to need a

lot more money invested to cover those expenses. So being frugal and saving

as much money as possible is actually going to serve

two different purposes here. Well, number one, the

less that you're living on the more of your paycheck

you're able to save up, and the more of your paycheck

you're able to save up, the more you're able to

contribute to that freedom fund, which will eventually be paying for all of your living expenses. And then second of all by spending as little money as possible

every single month, you actually don't need

to save up as much money to potentially live off of the interest or the growth of your money.

And we're going to go over

those exact numbers right now. Alright guys so step number two

that you have to follow here is going to be a tough one, but that is going to be saving 50 to 70% of your take home income and again, if you're looking to

retire by 30 years old, let's say you want to work from 20 to 30, and then not work for

the rest of your life, you're going to have to take

some drastic actions here.

And that is why you need to live off of a microscopic amount of money. And that's why step number

one is so important, by cutting down as much as possible on those monthly expenses. So people who are trying to do this, you're not going to see

them driving brand new cars, you're not going to see

them going on vacations, they're probably going to be,

you know, eating canned beans and doing campfires in the

backyard as summer entertainment. Not that there's anything wrong with that, but they are literally spending

as little money as possible, because they're focusing

on the long term picture of what they are trying to do. So people who are following

this FIRE movement are often aiming to save 30

times their annual expenses, and that will allow them to

withdraw about 4% per year without basically touching that principle and that is where that

4% rule comes into play.

And that is basically where you're able to draw from an account about 4% per year, and over a long period of

time based on the growth of that account and those investments, it shouldn't be chipping

away at the principle which should in theory

give you unlimited money. So what you're aiming

to do here is to lower your monthly expenses as much as possible.

Figure out what it costs

you to live per year, multiply that by 30, and then

save up that amount of money by saving 50 to 70% of your

paycheck every single week or month, or however often

you are getting paid. Alright so now the question

you guys have been waiting for, just how much money do

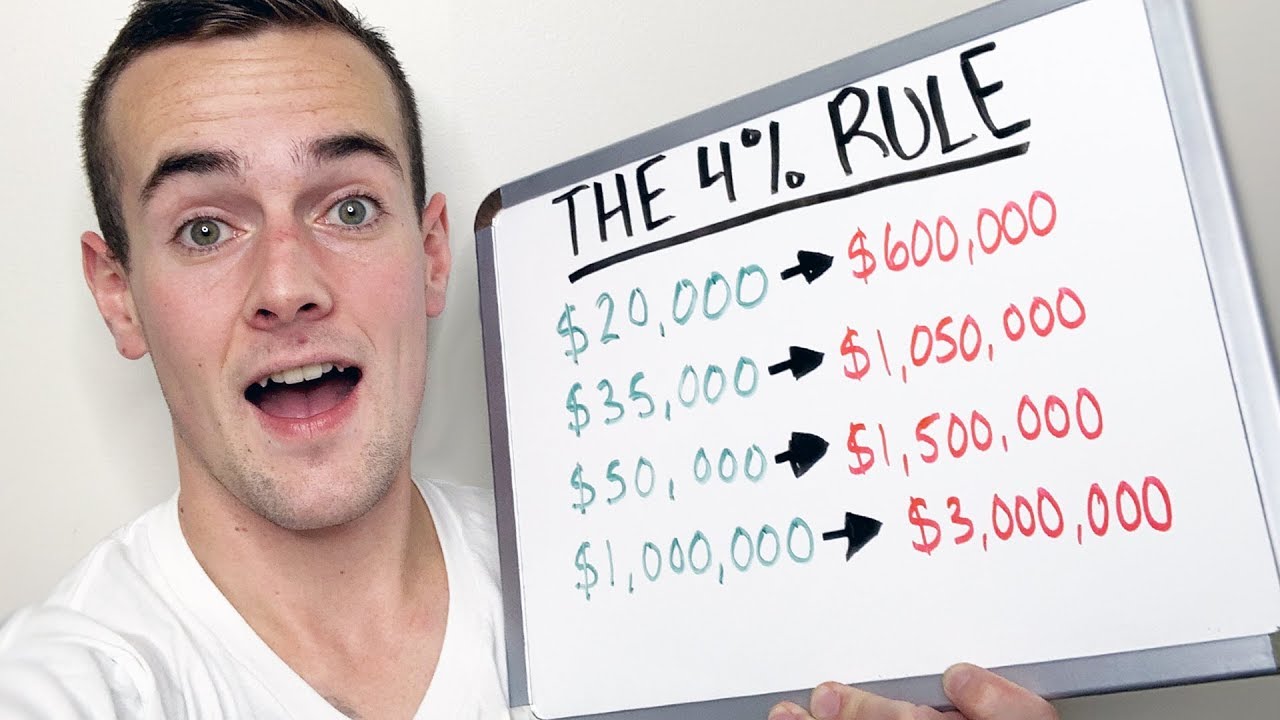

you need to have saved up and invested to live off of that money following the 4% rule. Well if your annual expenses

are $20,000 per year, they would recommend having 30 times that amount of money saved and

invested, so $600,000. If your annual expenses were $35,000, that number becomes 1.05 million. If you're somebody

spending $50,000 per year on your living expenses

you would need to have $1.5 million saved and invested,

and for the final figure here, if you spent $100,000 per

year on cars and housing and food and all of that,

you would need to have about $3 million to successfully

follow this strategy.

So I'm sure this goes without saying guys, the best way to follow the strategy and to reach that retirement as quickly as possible is going to be

to keep your monthly expenses as low as possible. And just to put it in

perspective for you guys, every additional $100

that you spend per month, if you follow this is

an additional $36,000 you need to have set

aside in that freedom fund to support that $100 of monthly spending. So if you're serious

about this and you want to retire at 30, or even younger, you are spending literally as little money as humanly possible. Alright so the final step

to following this strategy is going to be passively

investing in the stock market. So most people following this strategy are actually following

the Warren Buffett style of passively investing in index funds. And if you're not familiar,

index funds are basically a way for you to have diversified

exposure to the stock market. Where you're not essentially

picking what stocks are going to outperform,

you're just passively owning the entire market.

So people following this strategy are not out there trying

to beat the market, they are not stock

traders or stock pickers they simply passively invest

in these low fee index funds, one of the most popular ones being VOO or the vanguard 500 fund. And essentially what you are doing, is buying a small piece of the 500 largest publicly traded companies out there, and all the different

dividends those companies pay are all collectively put together, and then you earn a quarterly

dividend from that ETF.

And over the last hundred

years or so the stock market, on average, has returned

about eight to 10% per year. So if you were only drawing

4% from that account, based on historical data, you should never be

touching that principle over a long period of time. And that is how you would

be able to live off of 30 times your annual income, if you save that money and invest it. Now that being said that

is the perfect segue into the sponsor for this

video which is Webull. So if you guys are

interested in getting started with investing in the stock market, this is a totally commission

free broker out there, meaning you're not paying

any fees to please trades with them and you can

purchase the Vanguard 500 ETF that we're talking about in this video right on that Webull platform, and not only that, they're

willing to give you up to two completely free stocks just for opening up an account with them. Number one, if you open the account, you're going to get a free

stock worth up to $250, and then when you fund the account, you'll get an additional

stock worth up to 1000.

So if you do the math there, that is two completely free stocks worth up to $1,250. Now I am affiliated with Webull, so I do earn a commission in the process if you use my link, but

if you guys are interested in grabbing two completely free stocks that is going to be down

in the description below. So finally, the last

thing I want to do here is to put all of this together, and go through a real

example of how you could in fact follow this strategy and even retire by 30.

Now again, this is going to

require some very drastic saving because essentially you're trying to work for about 10 years of your life and then not have to work

for the rest of your life. So most people will never

be able to accomplish this, because of the amount of

sacrifice that is required, with that being said, let's go ahead and run

through the numbers now. So let's say you're earning

a salary of $75,000 per year from your job, and ideally,

you don't have any, you know school loans,

student loans, medical bills, or anything like that. So you haven't gotten

sucked into the consumerism and you don't have like a brand new car so your expenses are as low as possible.

And I know this sounds like

you know theoretical situation, but this was actually

about the same situation I was in, when I graduated

college I was 20 years old, now I was making about $68,000, so a little bit less, but I had no debts, I had no car payment,

and so I was somebody who could have potentially

followed this strategy. So after you pay your

taxes, your take home pay is going to be around $56,250. Now we know already in

order to pull this off, you need to save 50 to

70% of that take home pay in order to actually build up enough money to live off of that income. So we're going to assume

you are saving 70% of that take home pay. So you would need to live off of 30% of that post tax income, which

amounts to just over $16,000, or around $1400 per month.

Now, is that possible? It absolutely is. Is it easy? Absolutely not, you're certainly not going to be going out to the

bar and buying beers or going out to dinner,

you're probably going to be living in a tiny apartment driving an old car and eating at home for breakfast, lunch, and dinner. But if that type of

sacrifice is worth it to you for the long term picture, it is something you may

be willing to do yourself. So each year you would

be saving and investing a staggering amount of money, which is 70% of your take home pay

or just over a $39,000. And that is how you would

be able to pull this off, and assuming you kept that

cost of living the same at around $16,000, just over 16,000. your freedom number, or 30

times your annual expenses, would be just over $506,000. So, how long would it take

you to save up that money? Let's go ahead and answer that now.

Well if you took that

$39,375 per year of money that you are saving and

invested in the stock market, earning 8% return, and

as we said, historically, it's an eight to 10% so we're going to go on the conservative side, well in 10 years at 8%

return career you would have $570,408.40, meaning you could then, if you kept those living

expenses the same, following that 4% rule, not have to work for your

money past that point.

And just to circle back

guys what this really comes down to is the level

of sacrifice involved. Are you really willing to live

off of about $1400 per month, or do you want to have vacations and going out to get dinner

and things like that? So it's not people who are doing this that are out there traveling and dining it's people that are living

as frugal as possible and finding enjoyment

in other areas of life other than just, you know,

spending money on dining and things like that. Now, is this a strategy I

would personally follow? Probably not because I

am one of those people that enjoys traveling, I enjoy dining, and I do spend a little bit

more than the average person, so my freedom number would be

multiple millions of dollars, but instead I follow the

strategy of earning as much as possible and saving a

lot of that earned money, and then eventually allowing

that to supplement my income by having that interest

or the growth of my money paying for a lot of

those things that I want.

And believe it or not,

guys, there are honestly countless people out

there that have followed this exact strategy and

retired at 30 or less. One of the most well known people being Mr. Money Mustache, he has a whole blog where he documented this whole journey of becoming financially

independent and retiring early with both him and his wife. So I'm going to link up his blog down in the description below

as well as a couple of other stories about

people who have followed this exact strategy and

retired at 30 or less. So that's going to wrap

up this video guys, thanks so much for watching. If you're new to this channel, make sure you subscribe and

hit that bell for notifications so you don't miss future videos, and I hope to see you in the next one..

Retire Rich: 2023 Ultimate Planning Guide (Step-by-Step)

Jason 0 Comments Career after Retirement Retire Wealthy

– What's going on you guys. Welcome back to the channel. So in this video today, we're gonna be going over a ultimate guide to retirement planning in 2021. You already know I got my seltzer here. I gonna go ahead and

crack this bad boy open. And we're gonna get this

video started shortly. So at the end of the day, most

people do not want to spend the rest of their life working. And since your expenses don't

just magically disappear, when you turn 60 or 65 or

whatever that retirement age is you have to do things in order

to plan for your retirement. And so in this video, I'm

gonna go through exactly what you need to know to

start off this process of planning for retirement. This is going to include a

number of different topics. We're gonna talk about, how to tell when you can retire based on your level of income. We're gonna cover three primary ways that people derive

income during retirement, when to start saving for retirement, which is as soon as possible obviously, where to save for retirement? And we're also going to cover, how to make your retirement money last? Now real quick here, guys I just want to say thank

you to today's video sponsor which is T-Mobile.

We're gonna talk about

that more later on guys but I just wanna mention

here that T-Mobile offers their Essentials Unlimited 55 and up plan which is going to be

offering unlimited talk, text and data on two lines

at just $27.50 per line. It is a great option for people who are approaching retirement

age, who are looking to minimize those monthly recurring expenses. Compared to Verizon and AT&T

you can often save around 50% with T-Mobile. Not to mention guys, T-Mobile is the only wireless

company that offers a discount on the 55 and up plans regardless of what state you live in. Other companies like Verizon and AT&T only offer those discounted

plans in Florida. So you may wanna check that out. In addition, if you're thinking

about upgrading your phone and getting the latest 5G technology, 5G is included at no

extra cost with this plan. But more on that later. Now I'm definitely not looking

to waste your time here with this video guys. So I wanna go ahead and

identify who this video is for.

Well, mainly this video is geared towards people who are

approaching retirement age. You're probably not ready to retire but it's something that's on the horizon in the next 5 to 10 years. And you're wondering what things should you be aware of right now, and how can you get your ducks in a row for when you do approach

that retirement age. This video is also helpful

for those who are just looking to prepare for

retirement early on.

Even if you're in your

20s like me or your 30s, there's things you can start doing today that are gonna be relatively painless. And trust me, you're gonna

thank yourself later, when you have a lot of money set aside for your golden years. Now, many hours of research

did go into this video. So I just have three small

favors to ask you here, guys. First of all, if you are sitting there and watching this on your computer, go ahead and put your phone on silence and put it away for a little bit, because you wanna focus

all of your attention on this video, and not be distracted with all those social media apps, you can go back to those shortly. Also guys, make sure you pause the video and grab a pen and paper.

And if you need one, go ahead

and grab a beverage as well. We are gonna be here for a little bit but I promise to you that I'm gonna answer probably

every question you have about retirement planning in this video. So you're not gonna have to jump to like 10 different videos to get all

of your questions answered. Lastly guys, if you enjoy this video just go ahead and drop a like, it shows me that this

information was helpful and I'm not asking you

to like the video now but at some point, if you're

watching it and you say, "Hey, this was pretty helpful." That little thumbs up button

certainly does help out. Lastly, a few quick disclaimers

I have to make here.

I am not a financial advisor. This is not financial advice. You need to do your own research before investing in anything out there. Don't do what some guy on the

internet just tells you to do. I'm not here to sell you any products. I'm not selling any courses

or anything like that. And lastly, I have been

getting a lot of scam comments down below where people

are impersonating me. They're trying to get

people to send money. That is not me. I wanna put up two comments

on the screen here. This is a comment that's from me. And you can see the check mark and the different way that it looks versus this scam comment that

doesn't have those things. So if you're communicating with

someone down in the comments and it's me, make sure I

have that check mark in place otherwise you better

bet that is a scammer, and they're trying to take your money.

Hopefully YouTube does a

better job at policing this but for the time being, it

is utterly out of control. And I don't really know what else to do other than make this disclaimer

in every single video. That being said, guys,

let's get right into it and start off with when can you retire? And to be honest with you guys,

it's a pretty simple answer but the way of figuring this out is a little bit more complicated and we're going to cover that later.

But the truth is when

you're able to retire is when you no longer need

to rely on active income to pay for your expenses. So most people out there have a mortgage, they have car payments, they have different monthly expenses. And so in order to retire, you have to make sure that all

of those expenses added up, and even those unforeseen

expenses that you can plan for. Well, your level of income derived from your different investments needs to be enough to

cover those expenses. Otherwise you may have to go out there and get a different job to supplement your retirement income. And so for most people that may not be the ideal retirement scenario. So short answer here, guys, you can retire when your passive investment

income exceeds your expenses, but the longer answer is there's a calculation we're

gonna use to figure this out, that we'll discuss later in the video.

So next up, what are your different

options for retirement income? Well, this pretty much comes down to anything out there that

can make you money, but there's pretty much three main areas where people derive retirement income. The first one is your personal savings and your personal investments. So maybe you're somebody

who's worked a job for your entire life and you've been slowly

contributing to that 401(k). And then maybe you also

have some IRA accounts. Maybe you have a Roth

IRA or a traditional IRA.

And then beyond that, you might have a nest

egg with your savings. Maybe you have the taxable

brokerage account as well. And the goal is for

eventually all these things to be able to provide income for you to not have to work in

order to pay for your bills. Now, the second area

where people derive income for retirement is social security. However, we've certainly

heard a lot about this in recent years, and I don't

think it's such a safe thing especially for young people

to be reliant on that in the future because

social security is kind of in shambles right now

where we don't know how long it's going to last. However, if you are

approaching retirement age, that may be something you can count on for the time being is deriving income from social security. However, social security

alone, 90% of the time is not going to be enough

money to pay for your expenses unless you're living in like the smallest apartment in your entire city and you pinch every penny. And at least for me that's not my idea of a good retirement.

And just a couple of statistics I wanna share with you guys

here about social security, 40% of those who are 60

and above are 100% reliant on social security as a means of income. And so, like we said, here,

there's three different ways people typically derive income, but most people are just fully

reliant on social security which is something to be worried about. And if you're a younger

person watching this video, you don't want to put

yourself in that situation. Another surprising statistic here is that the social security trust fund based on the current rates is likely going to run out around 2035.

Now, are they gonna let

it run out entirely? Probably not. What they're gonna do is probably decrease payouts over time, which means that those who are reliant on that as income are gonna start making less and less money if they have to decrease those payouts. So that is why you really

don't wanna be in the situation where your reliant on this

social security income as a means to sustain yourself. And then lastly, the third source of retirement income for most people that's becoming less and less common is something called a pension.

Now pensions vary from company to company. In the past, it was

typically a percentage of your highest earning year

basically paid to you in perpetuity until you are passed away. But what they found is that these things are not very

profitable for companies. And it's very rare to

find any companies today that still offer this pension. But if you're an older

person watching this nearing retirement age, you may still have a pension plan to derive income during retirement.

So your best case scenario

here for retirement is that you're deriving income from these three different sources. Number one, personal savings

and personal investments. Number two, social security,

number three, your pension. That's like the perfect

scenario for retirement. However, unfortunately

only about 6.8% of people over age 60 are deriving retirement income from all three of those sources. So the vast majority of people

probably don't have pensions and some unfortunately don't

have any personal savings or personal investments. So that's the big picture right now. And that's why it's very

important to have your ducks in a row and start thinking

about this early on and planning that way. You can try to have a a

three-legged stool here where you're able to derive

income from multiple sources.

You don't want to be fully reliant on social security or fully

reliant on pension income or personal investments, personal savings. You wanna have different

things that are able to generate income for you

that way you're diversified. Because basically people

who are deriving income from one source are balancing

on a one-legged stool. It's not very stable. You wanna have multiple legs

to that stool, ideally three. And of course in that personal investments and personal savings

category, there's a lot of different things that

fit under this category. For most people, it's stocks and bonds but a lot of people also invest in things like real

estate or precious metals. And there's a lot of people who literally will

just put all their money in real estate, build up, you know a portfolio of 30 or 40 units. And then they live off of

that rental income cashflow. So there's many different

ways to skin a cat here, guys but just understand that

your goal here should be to derive money from

multiple different sources and have three legs to that stool. So next up here, guys, let's

answer the question of, when should you start

saving for retirement? Well, short answer as

soon as humanly possible.

Now, what I mean by this is when you're younger and

your expenses are lower. Let's say you're in

your 20s and early 30s. Maybe you don't have kids yet. Maybe you're still

living with your parents. This is your prime opportunity

to put as much money as you can into your 401(k), maxing out Roth IRA contributions, and basically holding onto

as much money as you can and putting it in

something that grows value. Because the main factor in how much money you have in retirement isn't based on how much

money that you invest.

It's how much time you

allow that money to grow. So even if you're in your

20s or 30s watching this, and you're thinking, "I don't really have a ton that I could set aside right now." It doesn't matter how much you put aside, the main factor is the amount of time that you allow that money to grow. So just for an example here, guys if you're looking to have $1

million in your retirement let's say your 401(k) for example you could invest just $300 per

month, over a 40 year period earning the average return

from the stock market. Or if you wanted to do it in 20 years, you would have to invest $1,750 per month. That's almost six times

more money to get you to the same result. So you can either invest

a smaller amount of money for a much longer time or you're going to have

to invest a lot of money for a shorter window of time. So the sooner you start,

the better off you are. And I highly encourage you to check out a compound interest calculator and play around with some of those numbers if you are a young person

watching this video.

If you're already close to retirement age and you didn't do these

things, don't worry. I still have more options for you that we're going

to discuss in a little bit. And again, it's important

to understand that truly it's never too late to start saving and investing for retirement. So even if you are in your

50 and you have no assets, you should still do something. You know, doing something is

better than doing nothing. It's gonna be a lot harder because you don't have that much

time to let your money grow, but it's never too late.

It's just important to

understand the sooner you start the better off you are. So now, let's talk about where you should be saving

money for retirement. And there's a pretty simple

process to follow here that most financial experts agree on and I'm going to teach

it to you right now. So the very first thing you should do before investing your

money in the stock market and opening up different

investment accounts is to set up an emergency fund. And this is just simply a liquid account. It sits there in a online savings account or a savings account at your bank or maybe a certificate of deposit. And so what you want

here is a rainy day fund. So what most experts

recommend is setting aside three to six months of

all of your expenses. So what you wanna do is sit

down on a piece of paper write down every one of your expenses, your car payment, your mortgage,

groceries, utility bills and come up with that figure. Let's say for most people maybe it's $3,000 per month

is their monthly expenses.

Well, I would encourage you to save up six times that expense

in a liquid emergency fund. So your very first step is to have let's say anywhere from

10,000 to $20,000 parked in a savings account

where it just sits there in case of emergency. And then you're not going

to invest that money. You just leave it sitting there. And if you end up taking

money out for an emergency like a car repair or a medical expense, you replenish that fund and

you keep that amount there. And of course, if your monthly expenses

are going up over time, you're going to want to

adjust your emergency fund accordingly to make sure you

keep enough money in there. So that's your very first

step is, begin saving up money for an emergency fund and

aim have three to six months of expenses sitting in a liquid account. The very next thing you should do after you have your emergency fund in place is to take advantage of any employer match with the 401(k).

So if you're not familiar, the 401(k) is an employer

sponsored retirement plan which allows you to take money pre-tax and put it away for retirement. And it also gives you

a pretty nice write-off on your tax return, which is

something else to consider. Now, I don't recommend

putting all of your money into the 401(k) because

it's hard to access it and you'd have to pay taxes and penalties to get that money out. However, if your employer

is offering a company match, you should maximize whatever

they're offering you because that's literally free money. So back before I was a

full-time YouTuber guys, I used to work for a utility company and they didn't have a

pension or anything like that, but they did have a employer match. So every dollar I would put in, they would match me with an

additional 50 cents up to 6%. So what I would do is I put 6% of my paycheck into my 401(k)

and then they matched me 50%. So I got another 3% for free. So, effectively 9% of my total pay was going into my 401(k) every

single week automatically.

So after you have your

emergency fund established, or at least started. You don't have to have

all that money there before you move to step two. You just want to kind of start that and begin putting a little bit over there every single week to build up that fund. The next thing is to take advantage of those employer 401(k) matches. After that, if you have any

high-interest debt, you know like personal loans, credit

card debt, things like that. You wanna pay that debt off next, because the average

return you're gonna see from the stock market is somewhere

around 8 to 10% per year. And so if you have high-interest debt, like let's say you have a

credit card with 25% interest, the most wise move you can

make financially is to pay off that debt because you're

paying way more in interest than you're gonna earn as a return. If you had $1000 invested and you're gonna make 10% in one year, you're going to make $100.

If you have a $1000 on a credit card at 25% interest over

the course of one year you'd pay like 250 in interest. So even though you could invest

that $1,000 and make $100 you're still paying 250 in interest. So overall it's a net loss. So if you have high-interest debt, you got to get that paid down first before you begin investing in other stuff, just because that's your

wisest move financially. So after you have your

emergency fund in place and after you maximize your employer match and then you pay off your

high-interest debt, if applicable the next thing to consider is an IRA.

And in particular, I like the Roth IRA. Assuming you're able to contribute to this based on your level of income. Now I'm not gonna get into

a whole thing here guys on Roth IRA versus traditional IRA. I could probably spend 30 minutes on an entire video talking about that. So for now, we're just gonna

cover some very basic stuff about the Roth IRA. With your 401(k) as mentioned, you're contributing pre-tax income and you get the write-off. However, down the line when

you draw out of that account that is when you pay taxes. With the Roth IRA, you're actually contributing

post tax income. So you've already paid taxes on it, meaning you don't get any write-off. However, if you follow

the rules and you know you start drawing from

that by a certain age you don't actually have to pay taxes on the growth of your money.

So it's a very powerful account and it allows you to grow

your wealth tax free. The other advantage of the Roth IRA is you can pull out your

contributions at any time. So if you were putting a $2,000

per year of contributions into that Roth IRA, every single year, you can pull out those

contributions at any time, tax free, penalty free. You just can't touch the earnings or the growth of your money. So let's say you're putting

money into a Roth IRA. And then 10 years later, you decide that you want to invest in a

business or something. You can pull that money out

and pull your contributions out and not have to worry

about penalties and taxes.

So I liked the Roth because it's flexible, you can choose where you put that money. You can put it in stocks,

bonds, precious metals there's all kinds of different Roth IRAs. And you have access to that money where you can take out your contributions, if you do need to access it. So now assuming that you have

the emergency fund in place, you're maxing out your 401(k), you've paid off high-interest debt, you've maxed out Roth IRA

contributions for the year. After that, that's when

I would put that money into a taxable brokerage account where you're able to invest that money, you're able to touch it

you're able to access it.

The only thing is you pay

taxes on your dividends and taxes on those capital gains. But for the most part, that is the generally agreed upon plan for where you should save

money for retirement, is in these different things

that you have control of. And this is all within that category of your personal savings

and personal investments. As far as your pension goes that's all based on your employer, most of them are not

offering any pensions today. However, if they offer it and it's something you

have to contribute towards, if you expect to stay with

that employer for a long time and make a career out of it,

that is definitely a wise move.

And then you automatically pay into social security if

you are a W2 employee. So that's not really something

you have any choice over. So now let's go ahead

and cover how much money that you're going to

need in order to retire. Well, it's kind of a moving target and it's going to change

based on your lifestyle. I mean, are you looking to live in a one bedroom apartment and

drive a ten-year-old vehicle and you know, eat canned

beans for a living? Or do you want to retire

on a beach in Miami? So it all depends based on your lifestyle.

But there is again, another

generally accepted calculation that financial experts use, to calculate necessary retirement income. And it's something called the 4% rule that I'm gonna teach you right now. Also guys, just a quick reminder, I know I mentioned this earlier, but if you have found any

value in this video so far, a like would certainly be appreciated. It helps this video to be

shared with more people. And if you have any thoughts or questions leave me a comment down below. But anyways let's talk

about this 4% rule now.

Now, as far as the math behind this goes, I'm not going to get into it. If you wanna watch,

there's plenty of videos about the 4% rule that we'll

go into a lot more detail but essentially it's a

very simple calculation. What you're going to do,

is you're going to multiply your desired retirement income by 25. So let's say for example you wanna have $40,000 per

year of income in retirement. If that's how much money you want, you want to multiply that by 25. And that will tell you a rough idea of how much money you should have in your savings and your investments in your personal investment

and savings accounts. So for example, if you

wanted $40,000 per year, you would multiply that by 25 and you would come to the conclusion that you're going to want

to have $1 million saved and invested in these different accounts in order to sustainably derive $40,000 per year from that account

without running out of money.

Now, if you wanna be a

little bit more conservative, there is the 3% rule which

is going to be a multiple of around 33, but anywhere

between 25 to 33 times, your desired annual retirement income is how much money you

should have set aside saved and invested for retirement. So obviously guys, the main thing here is the

less money that you need per month based on your lifestyle, the less money you need saved and invested and the sooner you can retire. That's where that whole

FIRE movement comes from or Financially Independent Retire Early, that's people who live off of

as little money as possible. They save as much as possible and they aim to be retired in their 30s. And they're able to accomplish that by living off of as

little money as possible. I did a whole video on this

called how to retire by 30. If you guys wanna check it out at the end I will include a link down below. So now what I want to

cover here is what to do, if you're somebody who

doesn't have 25 to 33 times their desired annual income in a savings or retirement account.

Maybe you're already in

your 50s or early 60s. And you're saying, "What am I gonna do? I don't have money that's just going to fall out of thin air to put in this account,

what options do I have?" Well, let's cover those right now. The main things that you can do are surrounded by things

that you can control. And the main thing you can

control is how much money you're actually spending

during your retirement. So essentially you have two options.

You can try to make more money or you can try to spend less money. Now I'm more of a fan of

the offensive approach here which is figuring out

how to make more money. And so let's talk about that now. The first thing you could

do is figure out some kind of side hustle that you wanna

start maybe in retirement or maybe you wanna do this

before retirement and save up extra money and take all

that money and invest it. I've done a lot of videos

about side hustles. We're not going to get into them here but just understand that

this right here, this laptop this provides a lot of

opportunities to make money.

And it's certainly not rocket science, and I know a lot of people who in their later years have started

YouTube channels and blogs and these different things that allow them to make extra money on the side. So the first thing you wanna consider is, "Hey, let me look into

starting a side hustle." Second of all, pretty simple, spend less money now, pre-retirement. That way you can save

more money to invest. So if you're in your 40s

or 50s, and let's say for example, you're driving

a brand new luxury car and you're watching this

video and you're realizing, "Oh crap, I'm not

preparing for retirement." Maybe you make some

small sacrifices today, that allow you to save

and invest more money. So maybe you trade that car in and you get an economy vehicle and you take that difference

in your monthly payment, and you put that into your

Roth or your 401(k) instead. Another option, pretty simple, spend less money in retirement. We're gonna cover that

more in a little bit. I'm gonna give you guys some

tips on how you can do that.

And then lastly, option number four not the best one, which

is delaying retirement. Maybe you wanna push it

until age 70, age 75, which will allow you

to stay working longer. It will allow you to contribute money towards retirement accounts

and investment accounts longer and allow that money to

have more time to grow before you have to start drawing. So now what I wanna cover

here is a rough idea of how long your retirement

money is going to last. And I don't wanna sound morbid here guys but the truth is, you want

your retirement money to last until you pass away. And then you also wanna make

sure you have enough money sitting there to cover medical bills, funeral costs, and things like that because most people just

don't wanna be a burden on their family when they pass away.

Where they're out of

assets, they're in debt and then their family

has to scrape together 10 or 20 grand for a funeral. So it's not something that

we like to think about or really talk about but it is something that's important to prepare for. And so your goal here should

be to have enough money that you can have your money outlive you and cover some of those costs and maybe have a little

bit of money to pass on to your family as well,

maybe towards, you know college expenses or things like that. But anyway, let me give you

a couple of pointers here on, how long that money will last in a couple of different

factors to consider. Well, first of all how

long your money will last is going to largely depend

on your investments. Some of them are lower risk and some of them are higher risk. And so if you're investing

in higher risk assets, they may be more volatile but you may also see greater returns. On the other hand, if

you're super conservative and let's say you only put your money in fixed income assets, you may find that you're not taking on enough

risk, and you could find that your money doesn't last

as long as you need it to.

So, one of the main things

you have to understand with retirement is that asset mix. And for most people, it's a

split between stocks and bonds. And so that's the main

thing you wanna focus on is that allocation. If you'll have too much money in stocks and not enough in bonds, you might be taking on too much risk and your portfolio could be very volatile, going up and down in value all

the time, stressing you out. If you're too low-risk you might not be growing

your money fast enough and it might run out too soon. So figuring out that asset

mix is very important. Now as far as that number goes, there's a couple of different

rules of thumb out there, but one that most people agree upon is the 110 or the 120 rule. And it's based on your life expectancy. So, I actually am a fan of the 120 rule, which basically means

you take your current age and subtract it from 120. And that tells you how

much money you should have in stocks and the rest should be in bonds.

So for example, I am 25 years old, I would take 120 minus 25,

and that leaves me with 95. That tells me that 95% of my money should be in stocks and

only 5% should be in bonds. Whereas if we take a 70

year old, for example we would take 120 minus 70,

and that leaves us with 50. And that tells us that

50% should be in stocks, 50% should be in bonds. Now, of course, guys that

is a very basic example and it doesn't take into account your unique personal situation. So for exact numbers I

would actually recommend speaking with a financial

advisor and you don't necessarily have to have them manage your money, you can pay them for a

one-time consultation where you're basically saying,

"Hey I want you to tell me what my allocation should be, and help me understand how

that changes over time." But by far that's one of

the most important factors to consider is your asset

mix or asset allocation? Now in general guys, that 4%

rule that we discussed earlier has been pretty successful,

and most people have found that it lasts them around 30 years, which is a pretty long retirement.

That's about how long most

people expect to be around once they retire. However, the success of that

4% rule is largely dependent on that asset allocation we discussed. Because if you're not

taking on enough risk, and you're only earning

a very small return, you're going to dwindle

that money a lot sooner. Another important factor

to consider is taxation. And this varies based on the types of accounts that you have. As mentioned earlier, the Roth IRA is an account

where you put your money in and you pay taxes on the way in. But when you draw from that account you don't pay any taxes. Whereas with the 401(k)

it's tax-free going in but when you come out, you're

actually going to pay taxes.

So this tax situation

is largely dependent on your own investment accounts. Maybe one person has all

of their money in a Roth and somebody else has all

of their money in a 401(k). Those are vastly different tax situations. And this is a scenario again

where a financial advisor can look at this for you, and help you with some tax planning. And you can understand what

are the tax implications associated with your

different investments. So now that you have a

general idea of the factors that will tell you how

long your money will last, let's talk about some different ways to make your retirement money last longer. So the first thing you can do to make your money last longer, which is getting more and more popular is something called downsizing. So most people end up having a home where they raise their kids. And let's say that you're still

together with your spouse. You may now be in this situation where you have this three or four bedroom house, you're paying to heat all those bedrooms.

And you're maintaining this big house, when you're only utilizing

like 25% of that space. Even if your mortgage is paid off, you're still paying for

utilities and landscaping and things that on a much

larger property than you need. So you could downsize into an apartment or downsize into a smaller house. That's becoming more and more popular with the goal of reducing

your fixed monthly expenses. Another option, going back

to the side hustle idea, maybe you Airbnb, a part of your home or you do one of your bedrooms

or something like that, to figure out how to generate

income from that unused space.

But downsizing is a very popular option. Another one is reducing

your fixed expenses like your car payment, as

well as things like your utility payment and things

like your phone bill. So this is where I wanna

talk more about our sponsor for today's video, which is T-Mobile, because they have specific wireless plans designed for people in

retirement to save you money on those fixed monthly costs. So, 55 and up customers who live anywhere in the United States, not just Florida are able to get two lines

of unlimited talk, text and data on T-Mobile's network,

starting at under $30 each.

Which if you have an existing phone plan you have a general idea

of what you're paying, and I can tell you guys right now I'm paying a heck of a lot

more than $30 per line. Now you might be wondering if you're getting some really

cheap plan in the process and the answer is no. In fact, it comes with a lot

of different bells and whistles and extra perks. For example, it comes with the industry's best scam protection, unlimited

3G mobile hotspot data, international texting, no

annual service contracts, your very own dedicated

customer service team, as well as additional

free items here and there and discounts every single

week through T-Mobile Tuesdays. So oftentimes if you

switch from a carrier like, AT&T or Verizon, over to

T-Mobile with this plan, you could save upwards of

50% every single month. And while it may not sound

like a lot of money upfront when you factor in that cost

over the next 20 or 30 years, these little things you

can do to save money on those monthly expenses

really are going to add up. So if you are interested

in those 55 plus plans through T-Mobile, switching

carriers is very easy.

If you're ready to make the switch, you just have to stop

into a T-Mobile store, or you can call 1800 T-Mobile or visit T-mobile.com/55, and I'll go ahead and

include links to all of that as well as the phone number down below, if you guys wanna go

ahead and take advantage of those discounted plans. Now another thing you can do

to make your retirement money last longer is falling

into that category of delaying your retirement. You can also delay taking social security, and this can lead to you having

a larger monthly benefit. So for every year that you wait, you're going to get an

additional 8% in social security, every single month. And if you wait until age 70

to start taking social security you can get up to 24%

more every single month. So if you can delay retirement, and delay taking your

social security benefit, that can result in

additional monthly income. Another great strategy is exactly what we're talking about here, which is having a retirement spending plan before you stop working.

So you do things in advance

to get your ducks in a row. You cut down on recurring monthly expenses like your phone bill,

maybe you take advantage of something like

T-Mobile's 55 and up plans. Maybe you downsize, or you

decide to Airbnb a spare room as us as a side hustle. You just start planning early on before you hit retirement

age, and then you think, "Okay, I haven't planned for this at all. Let's get something going." You're better off to plan in the beginning and get your ducks in the row early. Another suggestion that I have is utilizing credit card reward

points, because a lot of people in their later years want

to travel during retirement. We're in a unique situation right now with the global pandemic,

but once it's safe to travel, that's a popular thing

in your retirement age is seeing the world.

Well, if you're able to

effectively use credit cards and get free points for

travel or free miles, that's another way to get

more bang for your buck. And as long as you're not paying interest on those credit cards and you're paying them

off every single month, I would highly recommend utilizing

credit card reward points and bonuses for travel. Lastly, one of the

things that you can do is make investments in your health to make sure that you're

not having a lot of medical stuff coming up in retirement.

Hopefully you have some

plan for health insurance. So let's say now that worst case scenario, you're somebody who is

in retirement right now and you're slowly realizing that you're going to run out of money. You don't have enough for that 4% rule and maybe you only have

one leg to your stool, which is social security. What options do you have available to you, if you know, you're going to fall short? First of all, as covered

earlier, you can reduce expenses or pick up a part-time job or side hustle.

A lot of people in

retirement end up working 10 or 15 hours per week on the side. Number one for something to do, and number two, just to

have extra spending money. Another option is to tap

into the value of your home with a home equity line of