Category: Retire Wealthy

How To Retire At 30 Living Off Investments

Jason 0 Comments Retire Wealthy Retirement Planning

in order to live off of

your investments completely. And I know that the title of this video may sound crazy about retiring by 30, and there are a lot of people

out there selling a pipe dream of you can retire by 30

as long as you invest in this course, or go buy real estate and while that may work for some people I'm not here to sell you guys a course or to pitch you on any

kind of product like that. What we're going to

simply talk about here is how much money you need to have invested in order to live off of your investments and essentially not have

to work to earn your money.

And believe it or not, there's

actually countless people out there who have in fact

retired as early as 30 years old, by following this exact strategy

that I'm going to outline. So if this idea of retiring early and not having to work for your money is something that interests you. What I want to ask you

guys to do is go ahead and drop a like on this

video just show your support. I really do appreciate

that as it helps out with the algorithm and allows this video to get shared with more people. But what we're going to look

at in particular in this video is something called the 4% rule, and that essentially

shows you just how much money you need to have set aside, in order to live

off of your investments. Now you can in fact live off of different types of investments like real estate or the stock market for

example or a business that's providing income for you. But what we're going to use in this video as an example is a passive

stock market investment, and we'll show you exactly

how much money you need to have invested in order

to live off of that income.

So the goal here with this

strategy is to simply invest your money and have a large

amount of money invested and then you would

essentially be living off of the interest income or

the growth of that money without touching the principle. And as I'm sure you guys can imagine if you're not touching the principle or your initial investment, then your money could

foreseeably last forever. Now, the sooner you're able to retire is all based on how much

money you're able to save up and how little money you are

spending each and every month, and there's actually a

whole movement of people that are following this

exact strategy, and it's something out there called FIRE, and FIRE stands for financial

independence retire early. And there's a lot of

people who are doing blogs and videos and all kinds of

stuff about this concept, and there are countless

examples out there, of people who have retired

as early as 30 or even less.

By following these strategies. Alright guys so there's

basically three steps you have to follow in order to do this, and as I'm sure you can imagine, step number one is to be frugal or to spend as little money as possible, because ultimately what

you're looking to do is save and invest enough

money that the interest or the dividends, or

whatever the growth is pays for your monthly living expenses.

And as I'm sure you guys can guess if your monthly expenses

are $6,000 versus $3,000, you're going to need a

lot more money invested to cover those expenses. So being frugal and saving

as much money as possible is actually going to serve

two different purposes here. Well, number one, the

less that you're living on the more of your paycheck

you're able to save up, and the more of your paycheck

you're able to save up, the more you're able to

contribute to that freedom fund, which will eventually be paying for all of your living expenses. And then second of all by spending as little money as possible

every single month, you actually don't need

to save up as much money to potentially live off of the interest or the growth of your money.

And we're going to go over

those exact numbers right now. Alright guys so step number two

that you have to follow here is going to be a tough one, but that is going to be saving 50 to 70% of your take home income and again, if you're looking to

retire by 30 years old, let's say you want to work from 20 to 30, and then not work for

the rest of your life, you're going to have to take

some drastic actions here. And that is why you need to live off of a microscopic amount of money. And that's why step number

one is so important, by cutting down as much as possible on those monthly expenses. So people who are trying to do this, you're not going to see

them driving brand new cars, you're not going to see

them going on vacations, they're probably going to be,

you know, eating canned beans and doing campfires in the

backyard as summer entertainment. Not that there's anything wrong with that, but they are literally spending

as little money as possible, because they're focusing

on the long term picture of what they are trying to do.

So people who are following

this FIRE movement are often aiming to save 30

times their annual expenses, and that will allow them to

withdraw about 4% per year without basically touching that principle and that is where that

4% rule comes into play. And that is basically where you're able to draw from an account about 4% per year, and over a long period of

time based on the growth of that account and those investments, it shouldn't be chipping

away at the principle which should in theory

give you unlimited money. So what you're aiming

to do here is to lower your monthly expenses as much as possible. Figure out what it costs

you to live per year, multiply that by 30, and then

save up that amount of money by saving 50 to 70% of your

paycheck every single week or month, or however often

you are getting paid. Alright so now the question

you guys have been waiting for, just how much money do

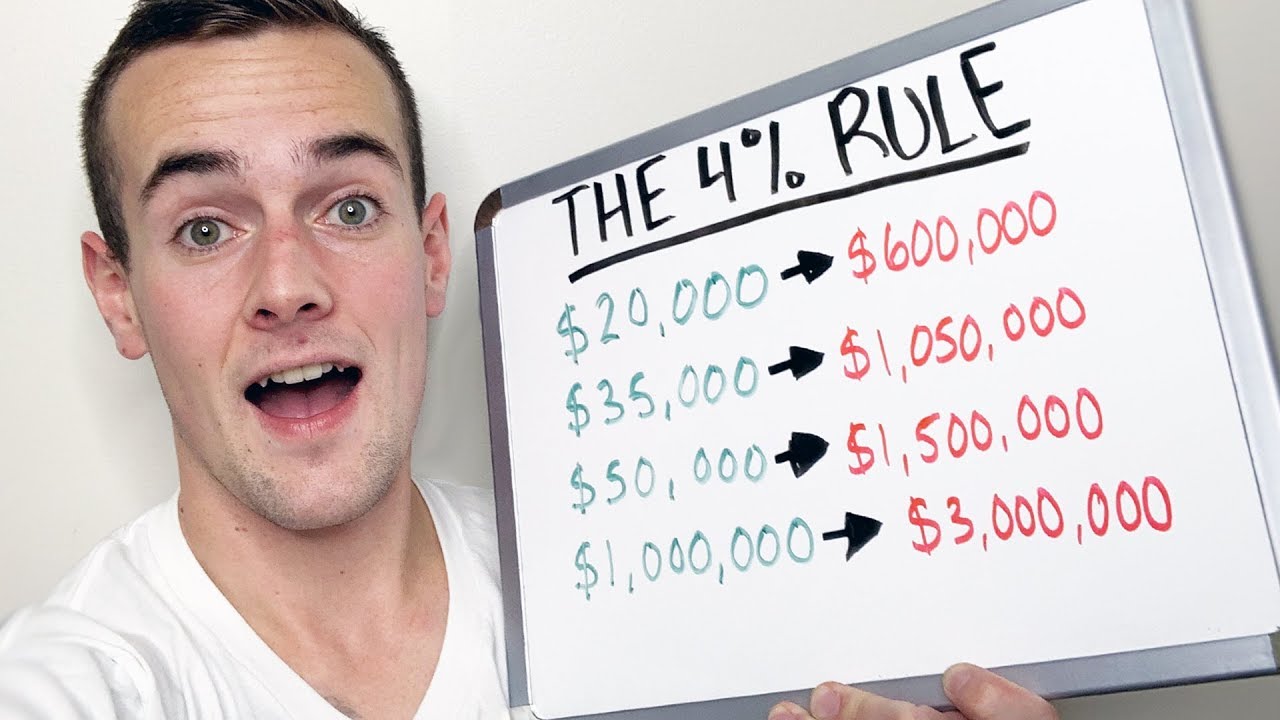

you need to have saved up and invested to live off of that money following the 4% rule. Well if your annual expenses

are $20,000 per year, they would recommend having 30 times that amount of money saved and

invested, so $600,000.

If your annual expenses were $35,000, that number becomes 1.05 million. If you're somebody

spending $50,000 per year on your living expenses

you would need to have $1.5 million saved and invested,

and for the final figure here, if you spent $100,000 per

year on cars and housing and food and all of that,

you would need to have about $3 million to successfully

follow this strategy. So I'm sure this goes without saying guys, the best way to follow the strategy and to reach that retirement as quickly as possible is going to be

to keep your monthly expenses as low as possible. And just to put it in

perspective for you guys, every additional $100

that you spend per month, if you follow this is

an additional $36,000 you need to have set

aside in that freedom fund to support that $100 of monthly spending. So if you're serious

about this and you want to retire at 30, or even younger, you are spending literally as little money as humanly possible. Alright so the final step

to following this strategy is going to be passively

investing in the stock market. So most people following this strategy are actually following

the Warren Buffett style of passively investing in index funds.

And if you're not familiar,

index funds are basically a way for you to have diversified

exposure to the stock market. Where you're not essentially

picking what stocks are going to outperform,

you're just passively owning the entire market. So people following this strategy are not out there trying

to beat the market, they are not stock

traders or stock pickers they simply passively invest

in these low fee index funds, one of the most popular ones being VOO or the vanguard 500 fund. And essentially what you are doing, is buying a small piece of the 500 largest publicly traded companies out there, and all the different

dividends those companies pay are all collectively put together, and then you earn a quarterly

dividend from that ETF. And over the last hundred

years or so the stock market, on average, has returned

about eight to 10% per year. So if you were only drawing

4% from that account, based on historical data, you should never be

touching that principle over a long period of time.

And that is how you would

be able to live off of 30 times your annual income, if you save that money and invest it. Now that being said that

is the perfect segue into the sponsor for this

video which is Webull. So if you guys are

interested in getting started with investing in the stock market, this is a totally commission

free broker out there, meaning you're not paying

any fees to please trades with them and you can

purchase the Vanguard 500 ETF that we're talking about in this video right on that Webull platform, and not only that, they're

willing to give you up to two completely free stocks just for opening up an account with them. Number one, if you open the account, you're going to get a free

stock worth up to $250, and then when you fund the account, you'll get an additional

stock worth up to 1000.

So if you do the math there, that is two completely free stocks worth up to $1,250. Now I am affiliated with Webull, so I do earn a commission in the process if you use my link, but

if you guys are interested in grabbing two completely free stocks that is going to be down

in the description below. So finally, the last

thing I want to do here is to put all of this together, and go through a real

example of how you could in fact follow this strategy and even retire by 30. Now again, this is going to

require some very drastic saving because essentially you're trying to work for about 10 years of your life and then not have to work

for the rest of your life. So most people will never

be able to accomplish this, because of the amount of

sacrifice that is required, with that being said, let's go ahead and run

through the numbers now. So let's say you're earning

a salary of $75,000 per year from your job, and ideally,

you don't have any, you know school loans,

student loans, medical bills, or anything like that.

So you haven't gotten

sucked into the consumerism and you don't have like a brand new car so your expenses are as low as possible. And I know this sounds like

you know theoretical situation, but this was actually

about the same situation I was in, when I graduated

college I was 20 years old, now I was making about $68,000, so a little bit less, but I had no debts, I had no car payment,

and so I was somebody who could have potentially

followed this strategy. So after you pay your

taxes, your take home pay is going to be around $56,250. Now we know already in

order to pull this off, you need to save 50 to

70% of that take home pay in order to actually build up enough money to live off of that income. So we're going to assume

you are saving 70% of that take home pay. So you would need to live off of 30% of that post tax income, which

amounts to just over $16,000, or around $1400 per month. Now, is that possible? It absolutely is.

Is it easy? Absolutely not, you're certainly not going to be going out to the

bar and buying beers or going out to dinner,

you're probably going to be living in a tiny apartment driving an old car and eating at home for breakfast, lunch, and dinner. But if that type of

sacrifice is worth it to you for the long term picture, it is something you may

be willing to do yourself. So each year you would

be saving and investing a staggering amount of money, which is 70% of your take home pay

or just over a $39,000. And that is how you would

be able to pull this off, and assuming you kept that

cost of living the same at around $16,000, just over 16,000.

Your freedom number, or 30

times your annual expenses, would be just over $506,000. So, how long would it take

you to save up that money? Let's go ahead and answer that now. Well if you took that

$39,375 per year of money that you are saving and

invested in the stock market, earning 8% return, and

as we said, historically, it's an eight to 10% so we're going to go on the conservative side, well in 10 years at 8%

return career you would have $570,408.40, meaning you could then, if you kept those living

expenses the same, following that 4% rule, not have to work for your

money past that point. And just to circle back

guys what this really comes down to is the level

of sacrifice involved. Are you really willing to live

off of about $1400 per month, or do you want to have vacations and going out to get dinner

and things like that? So it's not people who are doing this that are out there traveling and dining it's people that are living

as frugal as possible and finding enjoyment

in other areas of life other than just, you know,

spending money on dining and things like that.

Now, is this a strategy I

would personally follow? Probably not because I

am one of those people that enjoys traveling, I enjoy dining, and I do spend a little bit

more than the average person, so my freedom number would be

multiple millions of dollars, but instead I follow the

strategy of earning as much as possible and saving a

lot of that earned money, and then eventually allowing

that to supplement my income by having that interest

or the growth of my money paying for a lot of

those things that I want. And believe it or not,

guys, there are honestly countless people out

there that have followed this exact strategy and

retired at 30 or less. One of the most well known people being Mr. Money Mustache, he has a whole blog where he documented this whole journey of becoming financially

independent and retiring early with both him and his wife.

So I'm going to link up his blog down in the description below

as well as a couple of other stories about

people who have followed this exact strategy and

retired at 30 or less. So that's going to wrap

up this video guys, thanks so much for watching. If you're new to this channel, make sure you subscribe and

hit that bell for notifications so you don't miss future videos, and I hope to see you in the next one..

The Difference Between Wealth Management and Asset Management

Jason 0 Comments Retire Wealthy

OK so now you've been at JP Morgan for about 25 years. Yes. So

and now you run one of the most important parts of JP Morgan which as I say is the asset and wealth management business for

people that aren't that familiar with wealth management. What actually is wealth management and how is that different than

asset management. Great question. The two are often used interchangeably. But but but there they have distinctions. Asset

management business is where we manage money on behalf of individuals institutions sovereign wealth funds pension funds.

We manage them in mutual funds. We manage them an ETF. We manage them in single stock single bonds hedge funds private equity and

the like. And that is the heart of the fiduciary business that we run here at JP Morgan.

Wealth management is that plus

understanding someone's entire balance sheet. So for the individuals where we manage money we also help them with their

mortgage. We help them with a loan that they might need. We help them with their basic credit card. And so wealth management is

trying to help someone with their entire life both their assets and their liabilities their planning their gifting the legacy

that they want to leave for their families.

The 529 plans they need to prepare to get their kids to go through college. And

it's a great it's a great insight into people's you know entire journey. Now many organizations like J.P. Morgan to have wealth

management businesses some are bigger than some are smaller. But basically you're managing money for and doing other things for

wealthy people more or less.

Is that fairly right for wealthy people. Although you know many of the successful wealth

management firms today have figured out how to take all of those great learnings for what they do with very wealthy people and

also package them for people who are have their first paycheck. And they want to be able to save a little bit of money or want

to have access to things that maybe they wouldn't normally have. And so we've been able to take things like what we do for a

super wealthy family package it into a bite size where you walk into a chase branch and you're able to get some of that some of

the same advice. And so it's it's I think it's opening up the world to be able to help people. And you know the most important

thing is to be able to save early. And if someone can be there to help you through that you know that's that's one of the most

important things. If you look at an average investment in the world if you just look over the past 20 years take a balanced

portfolio.

It's about six point four percent average annual return for people that generally manage money. The problem is

most individuals actual return is less than 3 percent. So it's less than half of that. Why. Because they make emotional

decisions when markets are one way or another and they get caught up in the hype of things. And so it's super important to

have that advice as early on as we can give it. And I think you know that that's the rewarding part about about this business is

being able to try to help people through all of those different journeys that they have..

Retirement Planning Checklist

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Presenter 1>> Welcome to the CalPERS video Retirement Planning Checklist. In this session, we’re going to discuss a list of things you should be taking care of as you get ready for retirement. Before we get to the main presentation, let’s take care of some housekeeping items. To provide you with a future reference, and make your note taking easier, we’ve provided a presentation learning guide. You’ll see the link to the learning guide in the YouTube description box. Please note that due the large number of participants, although the chat feature is active, we won’t be able to respond to member questions during this presentation. If you have any questions, please contact us directly. Here’s the agenda for today’s presentation. We’ll start with things you’ll want to do one or more years away from retirement, and gradually work our way up to retirement and beyond. As we go through today’s presentation, we will reference several CalPERS forms and publications that you may be interested in, so here’s where you can find them. On our homepage at CalPERS.ca.gov, you’ll find the Forms & Publications column. Select the View All link at the bottom of the list to access a complete list of forms and publications which are shown in alphabetical order.

You can also filter by whether you’re an active member or a retiree. One of the publications you’ll want to review as you prepare for your retirement is Planning Your Service Retirement, Publication 1. It has a great deal of good information, including a checklist similar to what we’ll be reviewing here today. There is also a Retirement Planning Checklist on our website. Select the Active Members tab, then find the Resources column and select the Retirement Planning Checklist link.

Let’s start by looking at what you need to do about one or more years prior to your retirement. We encourage you to watch our Planning Your Financial Future video series available on the CalPERS YouTube channel. Financial security helps ensure you have enough money for the retirement lifestyle you want. Use our Planning Your Financial Future Checklist as a guide through this video series. For those who qualify for Social Security, visit our Social Security and Your CalPERS Pension page to learn how your Social Security benefits may be affected by your CalPERS retirement. If you haven’t already done so, sign up for a mySocial Security account at www.ssa.gov/myaccount. Here you can access your statement, review estimates of future Social Security retirement benefits, and more.

The service credit you earn is part of the calculation for your retirement benefit. Review your most recent account information in myCalPERS to make sure your service credit is accurate. You can also find a link to your most recent Annual Member Statement here. If you are a year or more away from retirement, use the Retirement Estimate Calculator in your myCalPERS account to estimate the amount of your pension and begin determining when you want to retire. It’s important to be prepared when you decide to take the big step into retirement. To get answers to most of your retirement questions, the Planning Your Retirement class is a great one to take if you are a year or even further from retirement.

Sign into myCalPERS and select Classes under the Education tab to enroll. If you think you may be eligible to purchase service credit, the first thing you should do is review the appropriate publication which provides the types of service credit available, eligibility for each type, and what is needed to submit the request. The publications are A Guide to Your CalPERS Service Credit Purchase Options, or for military time, the Military Service Credit Options publication. The publications can be found on our website. To find the cost of any available service credit purchases. First, log in to myCalPERS, go to the Retirement tab, select Service Credit Purchase, followed by the Search for Purchase Options button. You can also find the Service Credit Purchase link in the service credit box on the myCalPERS home page. Next, complete a series of questions to help determine which service credit purchase types you may be eligible for. Finally, the system will return the cost for any available service credit purchase options, at which point you can begin the purchase process if you choose to.

If you have a community property claim on your retirement account because of a legal separation or divorce, you must provide us with a copy of an acceptable court order that resolves the claim. It’s important to understand that a hold is placed on your account and retirement benefits cannot be paid until your community property issue is resolved. However, you shouldn’t wait to submit your application to retire. Waiting may affect the retirement date and other benefits. If you’ve been awarded a separate nonmember account, you may be eligible to retire and receive a monthly benefit for this as well. For more information, review our publication A Guide to CalPERS Community Property. You also may want to contact a financial planner for assistance with coordinating your CalPERS benefits with you overall retirement planning. Please remember that CalPERS does not provide financial planning services. Next is nine months prior to retirement.

If you're also a member of another California retirement system other than CalPERS, there are steps you need to take to ensure you receive all the benefits you’ve earned from each system. Reciprocity refers to an agreement between CalPERS and many other California public retirement systems that allow members to move from one retirement system to another within a specified time limit and possibly retain some valuable benefit rights such as your highest average pay in the calculation of your retirement.

Read our publication, When You Change Retirement Systems, for more information. If you have Social Security or other non-CalPERS income coming later after retirement, you might want to temporarily increase your monthly CalPERS income until those benefits begin. See if a temporary annuity is right for you by reviewing our temporary annuity publication. Moving on to five to six months before you retire. You should become familiar with the information needed to apply for retirement in the publication A Guide to Completing Your CalPERS Service Retirement Election Application, which is Publication 43. Begin to gather and make copies of the required documents you’ll need, such as a marriage license, or a birth certificate for a lifetime beneficiary. Refer to the Service Retirement Election Application for a complete list of required documents. If you apply for retirement online, you’ll be able to upload your documents into the system. If you choose to mail in the documents, only send us copies, never send originals. Always include your Social Security number or CalPERS ID on every document you submit. If you don’t know your CalPERS ID number, you can find it in your myCalPERS account under the My Account tab in the Profile section. Although an appointment isn’t required, if after taking the Planning Your Retirement class, you have specific questions about your own situation that weren’t answered during the class, you can schedule an appointment by logging on to your myCalPERS account.

You’ll find the Appointments link under the Education Resources tab. You determine how you want your taxes withheld. We can’t offer tax advice so you should check with your tax consultant or attorney to find out about the taxability of your overall retirement income. You can also find more information about your federal taxes on the Internal Revenue Service website at www.irs.gov. For your California taxes, you can go to the Franchise Tax Board website at www.ftb.ca.gov. If you plan on moving out of state, you are not required to pay California State taxes. However, you should check with the state you’re moving to find out what taxes they require and how they are to be paid. You cannot have out-of-state taxes taken out of your retirement check. And then three to four months prior to retirement. You can apply for service retirement online, in person, or by mail.

You can submit your retirement application no more than 120 days prior to your retirement. To file electronically, log in to myCalPERS. Go to the Retirement tab, select Apply for Retirement, and follow the steps for submitting your application and required documents online to CalPERS. We also have a video on our YouTube channel titled Your Online Service Retirement Application that will take you through the steps for completing and submitting your retirement application online.

There are a number of benefits to filing for retirement electronically. Easily and securely submit your application at your convenience, 24 hours a day. You can leave the online application and return at any point to complete it. Prior to submission, you can review and edit your information. You’ll receive confirmation that your application has been successfully submitted. You can upload additional required documents online. And, you can use the Electronic Signature to eliminate the notary requirement for the member signature. If you are unable or do not wish to complete your Service Retirement application online, you can submit the paper application at one of our regional office or by mail. If you bring your application to one of our Regional Offices, both you and your spouse’s or domestic partner's signatures can be witnessed by one of our representatives. If you choose to mail it in, you must have you and your spouse or domestic partners signatures notarized.

If you’d like assistance filling out your application, you can enroll in our class Your Retirement Application and Beyond. This class is available online through your myCalPERS account and is also taught by our regional office team members in virtual classes, and also in-person throughout the state. Find the next available instructor-led class in your area by logging in to your myCalPERS account or by calling us. Be sure you keep a copy of all forms and supporting documents for your records and future reference. Apply timely. Any delay in submitting your application could result in a delay of your first retirement check. If you have a deferred compensation plan such as a 401K, 457, or 403b, check with your plan administrator regarding distribution of your funds. Contact your health benefits officer or personnel office to determine your eligibility for continuation of health, dental or vision coverage into retirement. If applicable, check with your credit union, employee organization, insurance plan, or others to see if certain types of payroll deductions can be continued into retirement. So the next question is, what happens after you retire? As soon as your service retirement application is received, CalPERS will generate an Acknowledgment of Service Retirement letter.

This letter will confirm the retirement date you selected, your date of birth, your beneficiary’s date of birth, if applicable, the retirement option you selected, age at retirement, and the retirement formula along with other valuable information. About two weeks prior to your first check being issued, we’ll send you a First Payment Acknowledgement letter providing you with the date of your first retirement check, the gross amount you can expect to receive, and important income tax information. You’ll also receive an Account Detail Information sheet that provides what was included in your retirement calculation based on the payroll and service credit information posted in your account at the time your retirement was calculated. Finally, if you have CalPERS health coverage, you’ll receive two letters. The first letter will notify you that your health benefits as an active employee have been cancelled, and the second letter notifies you that your health coverage as a retiree has been established. You should keep all these letters, along with other CalPERS information you may have, with your important financial papers.

If you expect to have any adjustments to your retirement payment, you should allow four to six months for all final payroll to be processed for adjustments. An example of an adjustment would be a change in service credit or final compensation that was reported after your initial benefit was calculated. If after six months you haven’t received an adjustment that you think you’re due, you should send us a message through your myCalPERS account or give us a call at 888 CalPERS, which is 888-225-7377. You can find a list of mailing and direct deposit dates on our website.

If you applied timely, in most cases you should receive your first retirement check around the first part of the month following your retirement date. If you did not retire on the first of the month, your check will cover the period from your retirement date to the end of the month. After that, your check is mailed or direct deposited around the first of the month. This video will stay posted here on YouTube, so you can come back and catch what you might have missed. All our previous videos are also available on our YouTube channel. You’ll also have access to the link for the learning guide. Our presentation today was intended to provide you information on some steps you should be taking leading up to retirement. Please note that CalPERS is governed by the Public Employees’ Retirement Law. The information in this presentation is general. The Retirement Law is complex and subject to change. If there is a conflict between the law and the information presented in this presentation, all decisions will be based on the law. Later today, you’ll receive an email with a short evaluation. Please answer all the questions as it’s important for us to get your feedback to help us improve these presentations. Thank you for taking time out of your day to attend this presentation and have a great day.

Read More

Why This Investment System Can Help Retirees Worry Less About Their Retirement Plan

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

I want to share an investment system for retirees to hopefully assist you as you're thinking about and planning for your retirement we're also going to look at how to prepare your retirement for the multiple potential potential economic Seasons that we may be headed into so we want to look at the multiple seasons and then the Easy System that's going to help lower taxes and then lower risk as well now if I haven't met you yet I'm Dave zoller and we help people plan for and Implement these retirement strategies really for a select number of people at streamline Financial that's our retirement planning firm but because we can't help everyone we want to share this with you as well so if you like retirement specific videos about one per week be sure to subscribe so in order to create a proper investment plan in system we want to make sure that we build out the retirement income plan first because without the income plan it's much harder to design the right investment strategy it's kind of like without the income plan it's like you're guessing at well 60 40 portfolio sounds good or you know May maybe this amount in the conservative bucket sounds reasonable you already know and and you feel that as you get close to retirement that goal of just more money isn't the the end-all goal that we should really be aiming for for retirement it's more about sustainability and certainty and then really the certainty of income and possibly less risk than before the last 30 years uh the things that you did to be successful with the financial side are going to look different than the next 20 or 30 years now if you need help defining the the income plan a little bit then look at the DIY retirement course below this video now once you do Define your goals for retirement and then the income needed to achieve those goals then creating the investment system becomes a lot easier and within the investment plan we really know that we can only control three things in all three things we actually want to minimize through this investment system the first thing we can minimize or reduce is how much tax you pay when investing we had a a client who was not a client of streamline Financial but of a tax firm coming to the the CPA firm in March to pick up his tax return and he was completely surprised that he had sixty thousand dollars of extra income on his tax return that he had to pay tax on right away before April 15th and it was due to the capital gains being recognized and other distributions within his investment account and he said but I didn't sell anything and the account didn't even go up that much last year and I got to pay tax on it but he was already in the highest tax bracket paying about close to 37 percent on short-term capital gains and dividends and interest so that was an unpleasant surprise and we see it happen more often than it should but this can really be avoided and here's two ways we can control tax so that we don't have to have that happen and really just control tax and pay less of it is the goal and I'll keep this at a high level but it'll get the the point across number one is the kinds of Investments that you own some are maybe funds or ETFs or individual uh equities or things like that the funds and ETFs they could pass on capital gains and and distributions to you each year without you even doing anything without you selling or or buying but it happens within the fund a lot of times now we would use funds and ETFs that are considered tax efficient so that our clients they can decide when to recognize gains rather than letting the fund company decide now the second way is by using a strategy that's called tlh each year there's many many fluctuations or big fluctuations that happen in an investment account and the strategy that we call tlh that allows our clients that's tax loss harvesting it allows them to sell an investment that may be down for part of the year and then move it into a very similar investment right away so that the investment strategy stays the same and they can actually take a write-off on that loss on their taxes that year now there's some rules around this again we're going high level but it offsets uh you know for that one client who are not a client but who had the big sixty thousand dollars of income he could have been offsetting those capital gains by doing tlh or tax loss harvesting that strategy has really saved hundreds and thousands of of dollars for clients over a period of years so on to the next thing that we can control in our investment plan and that's cost this one's easier but many advisors they don't do it because it ends up paying them less now since we're certified financial planner professionals we do follow the fiduciary standard and we're obligated to do what's best for our clients so tell me this if you had two Investments and they had the exact same strategy the same Returns the same risk and the same tax efficiency would you rather want the one that costs 0.05 percent per year or the one that costs 12 times more at point six percent well I know that answer is obvious and we'd go with a lower cost funds if it was all the same low-cost funds and ETFs that's how we can really help reduce the cost or that's how you can help reduce the cost in your investment plan because every basis point or part of a percentage that's saved in cost it's added to your return each year and this adds up to a lot over time now the last thing that we want to minimize and control is risk and we already talked about the flaws of investing solely based on on risk tolerance and when it comes to risk a lot of people think that term risk tolerance you know how much risk can we on a scale of one to ten where are we on the the risk factor but there's another way to look at risk in your investment strategy and like King Solomon we believe that there's a season for everything or like the if it was the bird song There's a season for everything and we also believe that there's four different seasons in investing and depending on what season we're in some Investments perform better than others and the Four Seasons are pull it up right now it's higher than expected inflation which we might be feeling but there's also a season that can be lower than expected or deflation and then there's higher than expected economic growth or lower than expected economic growth and the goal is reduce the risk in investing by making sure that we're prepared for each and every one of those potential Seasons because there are individual asset classes that tend to do well during each one of those seasons and we don't know nobody knows what's really going to happen you know people would would speculate and say oh it's going to be this or this or whatever might happen but we don't know for sure that's why we want to make sure we just have the asset classes in the right spots so that the income plan doesn't get impacted so the investment system combined with the income system clients don't have to worry about the movements in the market because they know they've got enough to weather any potential season I hope this has been helpful for you so far as you're thinking about your retirement if it was please subscribe or like this video so that hopefully other people can be helped as well and then I'll see you in the next one take care thank you

The 4 phases of retirement | Dr. Riley Moynes | TEDxSurrey

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Transcriber: Zsófia Herczeg

Reviewer: Peter Van de Ven Everyone says you have to get ready

to retire financially. And of course you do. But what they don’t tell you

is that you also have to get ready psychologically. Who knew? But it’s important

for a couple of reasons. First, 10,000 North Americans

will retire today and every day for the next 10 to 15 years. This is a retirement tsunami.

And when these folks come

crashing onto the beach, a lot of them are going to feel

like fish out of water without a clue as to what to expect. Secondly, it’s important

because there is a very good chance that you will live one third

of your life in retirement. So it’s important that you have

a heads up to the fact that there will be significant

psychological changes and challenges that come with it. I belong to a walking group

that meets early three mornings a week. Our primary goal is to put

10,000 steps on our Fitbits, and then we go for coffee

and cinnamon buns – (Laughter) more important. (Laughter) (Applause) So as we walk, we’ve gotten into the habit

of choosing a topic for discussion. And one day, the topic was, “How do you squeeze

all that juice out of retirement?” How's that for 7:00 in the morning? So we walk and we talk, and the next day,

we go on to the next topic.

But the question stayed with me because I was really having

some challenges with retirement. I was busy enough,

but I really didn’t feel that I was doing very much

that was significant or important. I was really struggling. I thought I had a pretty good idea of what success looked like

in a working career, but when it came to retirement,

it was fuzzier for me. So I decided to dig deeper. And what I discovered was

that much of the material on retirement focuses on the financial

and/or the estate side of things. And of course, they’re both important

but just not what I was looking for. So I interviewed dozens

and dozens of retirees, and I asked them the question, “How do you squeeze

all the juice out of retirement?” What I discovered

was that there is a framework that can help make sense of it all.

And that’s what I want

to share with you today. You see, there are four distinct phases that most of us move through

in retirement. And as you’ll see,

it’s not always a smooth ride. In the next few minutes, you’ll recognize

which phase you’re in if you’re retired, and if you’re not, you’ll have a better idea

of what to expect when that time comes. And best of all, you’ll know

that there is a phase four – the most gratifying,

satisfying of the four phases – and that’s where you can squeeze

all the juice out of retirement.

Phase one is the vacation phase,

and that’s just what it’s like. You wake up when you want,

you do what you want all day. And the best part

is that there is no set routine. For most people, phase one represents

their view of an ideal retirement. Relaxing, fun in the sun – freedom, baby. (Laughter) And for most folks, phase one

lasts for about a year or so, and then, strangely,

it begins to lose its luster. We begin to feel a bit bored. We actually miss our routine. Something in us seems to need one. And we ask ourselves, “Is that all there is to retirement?” Now when these thoughts and feelings

start to bubble up, you have already moved into phase two. Phase two is when we feel loss, and we feel lost. Phase two is when we lose the big five – significant losses

all associated with retirement. We lose that routine. We lose a sense of identity. We lose many of the relationships

that we had established at work. We lose a sense of purpose. And for some people,

there is a loss of power.

Now, we don’t see these things coming. We didn't see these losses coming in

because they happened all at once. It’s like, poof, gone. It’s traumatic. Phase two is also when we come

face to face with the three Ds: divorce, depression and decline – both physical and mental. The result of all of this is that we can feel

like we’ve been hit by a bus. You see, before we can

appreciate and enjoy some of the positive aspects

associated with phase three and four, you are going to, in phase two, feel fear, anxiety

and quite even depression.

That’s just the way it is. So buckle up and get ready. Fortunately, at some point,

most of us say to ourselves, “Hey, I can’t go on like this. I don’t want to spend the rest of my life, perhaps 30 years, feeling like this.” And when we do, we’ve turned the corner to phase three. Phase three is a time of trial and error. In phase three, we ask ourselves, “How can I make my life meaningful again? How can I contribute?” The answer often is to do things

that you love to do and do really well. But phase three can also deliver

some disappointment and failure. For example, I spent a couple of years

serving on a condo board until I finally got tired

of being yelled at.

(Laughter) You see, one year the board decided

that we were going to plant daffodils rather than the traditional daisies. (Laughter) And we got yelled at. Go figure. I thought about law school,

thinking perhaps of becoming a paralegal. And then I completed a program

on dispute resolution. It all went nowhere. I love to write. So I created a program

called “Getting started on your memoirs.” That program has met

with “limited success.” (Laughter) It’s been a rocky road for me too,

and I told you to buckle up. Now, I know all this can sound bad. But it’s really important to keep trying and experimenting

with different activities that’ll make you want

to get up in the morning again because if you don’t, there’s a real good chance

of slipping back into phase two, feeling like you’ve been hit by a bus.

And that is not a happy prospect. Not everyone breaks through to phase four, but those who do

are some of the happiest people I have ever met. Phase four is a time

to reinvent and rewire. But phase four involves

answering some tough questions too, like, “What’s the purpose here?

What’s my mission? How can I squeeze

all the juice out of retirement?” You see, it’s important that we find

activities that are meaningful to us and that give us a sense

of accomplishment. And my experience is that it almost always

involves service to others. Maybe it’s helping a charity

that you care about. Maybe you’ll be like the old coots. (Laughter) (Applause) Yeah. These folks took a booth

in the local farmers market and were prepared to give their advice

based on their vast years of experience to anyone who came by.

So one of their first visitors was a kid

who wanted help with his math homework (Laughter) on his tablet. (Laughter) They did the best they could. Or maybe you’ll be like my friend Bill. I met Bill a few years ago

in a 55 plus activity group. In the summer, we golf together

and walk together and bicycle together. And in the winter, we curl. But Bill had this idea that we should exercise

our brains as well. He believed that there was

a tremendous pool of expertise and experience in our group, and so he approached a number of folks and asked if they would volunteer to teach some of the things

that they love to do to others.

And almost invariably, they agreed. Bill himself taught two sessions, one on iPads and one on iPhones, because we were smart enough to know

that a number of our members had been given these things

as gifts at Christmas (Laughter) by their children, and that they barely knew

how to turn them on. The first year, we offered nine programs,

and there were 200 folks signed up. The next year, that number

expanded to 45 programs with over 700 folks participating. And the following year,

we offered over 90 programs and had 2100 registrations. Amazing. (Applause) That was Bill. Our members taught us

to play bridge and mahjong. They taught us to paint. They taught us to repair our bicycles. We tutored and mentored local school kids.

We set up English-as-a-second-language

programs for newcomers. We had book clubs. We had film clubs. We even had a few golf clubs. Exhausting but exhilarating. That’s what’s possible in phase four. And do you remember the five losses

that we talked about in phase two? The loss of our routine and identity and relationships and purpose and power? In phase four, these are all recovered. It is magic to see, magic. So, I urge you to enjoy

your vacation in phase one. (Laughter) Be prepared for the losses in phase two.

Experiment and try as many different

things as you can in phase three, and squeeze all the juice

out of retirement in phase four. (Applause).

5 Best Fidelity Funds to Buy & Hold Forever

Jason 0 Comments Retire Wealthy Retirement Planning

today we're going to talk about the five best fidelity funds to buy and hold forever hi if you're new to the channel my name is tay from financial tortoise where we learn to grow our wealth slow and steady in order to guide our conversation i'm going to use the three fund portfolio strategy to frame the fidelity funds i'm going to recommend in this video the three fund portfolio is one of the most popular do-it-yourself investment strategies and as the name implies it's made up of three simple funds most often an equities fund an international fund and a bond fund so all the funds i'm going to recommend today will fit into at least one of these slots the first fidelity fund you want to buy and hold forever is fidelity's u.s bond index fund fxnax it tracks the bloomberg barclays u.s aggregate bond index which is composed of investment-grade government bonds corporate bonds and mortgage-backed securities it holds approximately 8 400 bonds the top issuers are the u.s treasury or issuers of mortgage-backed securities like fannie mae and freddie mac it has an expense ratio of 0.025 percent which means if you have 10 000 invested in fidelity us bond index fund you're essentially paying 2 dollars and 50 cents for fidelity to manage this fund for you the fund started in 1990 and since then its average annual total return has been 5.33 percent so what are bonds and why do you need them in the simplest term bonds or loans when you buy bonds you're essentially loaning money to someone in this case to a company or a government agency and they're a very important addition to a well-constructed investment portfolio because of how different they are from stocks a good analogy i like to use to frame stocks versus bonds is this think of stocks as your core wealth building engine without it you aren't really going anywhere and bonds are like your brakes without it you could drive yourself off the road when you have bonds in your portfolio it helps to smooth out your investment ride because though they have lower returns they have less volatility during times of market crash where your stock investments can dip by 20 to 30 percent your bond investments will hold steady and ensure your right is so rocky so in order to help you smooth out your investment right you want to start adding them to your portfolio as you get closer to retirement age and if you're invested in fidelity consider fidelity u.s bond index fund as your core bond holding in your portfolio the second fidelity fund you want to buy and hold forever is fidelity total international index fund ftihx the fund tracks the msci all-country world index excluding the united states it represents approximately 5 000 international companies the top companies in this fund are made up of companies like taiwan semiconductor nestle and asml holdings it has an expense ratio of 0.06 percent which means that if you have 10 000 invested in ftihx you're essentially paying six dollars for fidelity to manage this fund for you the fund started in 2016 and since then its average annual total returns has been 5.99 what the fidelity total international index fund will do for you is provide you exposure to the international market outside the united states exposure to different countries sectors and even currencies and we can look at what happened to the japanese stock market as a lesson on why we might want to hold an international fund at the end of 1989 the japanese stock market's capitalized value was considered the largest in the world the nikkei 225 index the index of 225 largest publicly owned companies in japan reached an all-time high of close to 40 000.

Sadly 22 years later the nikkei was under 8 500 and to this day has yet to reach its all-time high again but satur is a japanese investor who failed to invest in international stocks outside of japan the us-based companies are currently the world leader in market capitalization and revenue but who can confidently say that will stay like that in the future it would be unfortunate but the same thing could happen to the u.s stock investors i personally still have strong confidence the u.s economy and u.s based companies as a whole but i also have to continuously check my assumptions financial writer larry swegel had a saying never treat the highly likely as certain and the highly unlikely as impossible as you get more comfortable with the international market you can start adding them to your portfolio and the fidelity total international index fund is a great option to represent your international holdings the third fidelity fund you want to buy and hold forever is fidelity zero total market index fund fzrox the fund tracks fidelity's in-house fidelity u.s total investable market index it represents approximately 2 700 u.s based companies the top holdings in this fund are apple microsoft and amazon it has an expense ratio of zero percent yes you heard me right zero dollars to invest in fidelity zero total market index fund thus the zero in its name the fund started in 2018 and since then its average annual total returns has been 11.82 the fidelity zero total market index fund is a total market index fund which means it tracks the total u.s stock market so this will be a great option as your core equities holding in your three fund portfolio however there are a couple things i do want to note with this fund especially in comparison to the two other equities options i'll cover here in a bit one is the fact that the index it is tracking is fidelity's in-house index fidelity u.s total investment market index this necessarily isn't a bad thing but there are actually more than 2 700 publicly traded companies in the united states than what this fund represents what this fund has done is exclude really small companies from its index in a big scheme of things this doesn't make that much of a difference in performance since the representation is based on market capitalization so the excluded companies would only represent maybe one percent or even less than that of the total fund but this is still something to note the total market here isn't quite the total market a second item to note with the fidelity zero total market index fund is the fact that you can't transfer your shares to another firm without selling your holdings and when you sell your holdings you have to pay taxes on your capital gains the fidelity zero total market index fund was designed with zero percent expense ratio in order to gain more customers so fidelity doesn't want you to move your money to a different firm and this limitation creates that barrier paying zero percent is nice but you won't understand that free comes with some strings attached but if you're planning to stay with fidelity for life fidelity zero total market index fund is a great equities fund to hold the fourth fidelity fund you want to buy and hold forever is fidelity total market index fund fskax the fund tracks the dow jones u.s total stock market index it represents approximately 4 000 u.s based companies the top holdings in the fund are apple microsoft and amazon essentially the same as fidelity zero total market index fund it has an expense ratio of 0.015 percent which means that if you had 10 000 invested in fidelity total market index fund you're essentially paying 1.50 for fidelity to manage this fund for you the fund started in 1997 and since then its average and annual total return has been 8.29 it's fidelity's original total market index fund prior to the introduction of fidelity zero total market index fund and fidelity total market index fund does exactly what his name implies invest in the total u.s stock market essentially every u.s based companies out there when it comes to investing in the stock market the key principle you want to abide by is diversification many people tend to think the only way to make money in the market is to beat the market by either selecting good stocks or good actively managed mutual funds unless you're a professional investor with hundreds of analysts working for you around the clock analysts who are constantly interviewing and researching companies and industries we can't win in the stock picking or fun picking game the odds are just stacked too high against the individual investor so the best strategy to beat wall street is to just track the market and at the lowest cost and fidelity total market index fund is a great fun to hold as your core equity is holding in your portfolio if you want more flexibility from the fidelity zero total market index fund the fifth fidelity fund you want to buy and hold forever is fidelity 500 index fund the fund tracks the s p 500 index which represents the 500 largest publicly traded companies in the united states at the time of this video there are exactly 508 publicly traded companies in this fund the top holdings in this fund are apple microsoft and amazon essentially the same as fidelity zero total market index fund and fidelity total market index fund not a surprise given the company representation is based on market capitalization and these big companies represent a good percentage of the market as a whole it has an expense ratio of 0.015 percent same as fidelity total market index fund so if you have ten thousand dollars invested in fidelity 500 index fund you're essentially paying dollar fifty for fidelity to manage the fund for you the fund is the oldest of the bunch it started in 1988 and since then its average annual total returns has been 10.66 percent when most people talk about the stock market they're most often referring to the standard and poor 500 not the total market index and the reason is because it's so much older it was created in 1926 when it began tracking 90 stocks and in 1957 the list expanded to 500 and for the past century it has been the go-to index to represent the stock market when you turn on any financial news reporters are always discussing how the s p 500 is up 50 points or down 100 points it essentially represents the 500 largest u.s corporations weighed by the value of the market capitalization and because it's weighted by market cap though there are approximately 4 000 publicly traded companies in the united states total these 500 stocks represent about 80 to 85 percent of market value of all u.s stocks and the weight within the index automatically adjusts based upon the changing stock prices to this day the s p 500 remains a standard to which professional mutual fund managers and investment firms compare their returns against so if you want your equities holding to match the performance the largest u.s stocks since they're essentially what moves the market hold fidelity 500 index fund as your core equities holding but i do want to say this whether you choose the fidelity 500 index fund the fidelity total market index fund or the fidelity zero total market index fund as your core equities holding you really can't go wrong with any one of them they're all great funds you just want to understand exactly what you're buying that's it guys i know i normally advocate for vanguard funds but sometimes you may not have the ability to choose the investment firm that you want because maybe your employer doesn't offer it that was the case for me and therefore most of my 401k is actually invested in fidelity fidelity is a great investment firm if you're looking to invest with them pick any of the five that i mentioned here and you can't go wrong if you'd like to learn more about the three fund portfolio and why you might want to consider it as your strategy check out my video here thank you guys for watching until next time all the best

Read More

Wealth Transfer Prophecy Part 2. (The Wealth of the Wicked will be Given to the Righteous)

Jason 0 Comments Retire Wealthy

The Wealth of the Wicked will

be Given to the Righteous Wealth Transfer Prophecy, Part 2. This is the second part of the wealth transfer

prophecy, as we mentioned in the first video, God will use certain cryptocurrencies as

instruments to transfer wealth to his people. The first currencies that will be used in this phase

are Luna Classic, Shiba Inu, and Bitcoin. LUNC will rise first, and then SHIB, during the process

BTC will fall and rise a couple of times as well. This will allow God's people to place limit

orders, to buy BTC when the price falls to almost $1 per Bitcoin. LUNC, SHIB, and BTC will

be the first ones to provide opportunities, due to the rises and falls these coins

will have.

The prices to sell the coins in the sell limit orders, are the prophetic

prices made known by God through His prophets, as well as by His people who received visions

and dreams, granted by the outpouring of His Holy Spirit. Once the first phase is

finished, and after receiving profits, the prophecies point to buy the XRP and XLM

coins, which will definitely be one of the best investments to make, this is because

in the future XRP will be backed by gold, and XLM by silver. We should also point out, that

the prophetic word emphasizes the need to invest in real estate, agricultural land, goods,

properties, houses, buildings, facilities, etc, because in the future there will come

a time known as crypto winter, a period in which the entire global financial system,

including cryptocurrencies, will be down. In other words, prices will fall to the

ground, whose values will be too low, to be able to buy the necessary food,

which will be extremely expensive. Once the crypto winter time is over, God will

cause a large group of cryptocurrencies to rise in price greatly, and they will reach a very high

value in the future.

This is why God reveals to his children that when the cryptocurrencies

fall in value, whose prices will be very low during the crypto winter time, then, it will be

the right time to buy certain cryptocurrencies, whose values will be multiplied greatly in

the future. At the moment, we do not know yet, how many weeks, or months the coming future crypto

winter period will last. For this reason, it is essential to acquire agricultural fields and real

estate, one to produce food, and the other as a means to preserve profits. We remind you that all

the links you will need to learn, key information, prophetic prices, details, etc, will be in

the description of the video.

God bless you..

Read More

Do Withdrawal Rates Make Sense for Retirement?

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

As you plan your retirement, one of the biggest questions that comes up is how much can I afford to spend each year, and how can I be sure that I won't run out of money if I spend at a certain rate? And a lot of people look to a withdrawal rate to help them figure that out, in other words, they might say, Maybe I can spend 4% or 3%, and that way I would have enough money to last for the rest of my life, but I think there are a lot better ways to go about that, so I wanted to review those with you and point out some of the issues, and hopefully this way you see what you might be missing out on if you use a withdrawal rate and you don't have to waste any time obsessing over what exactly is the perfect rate…

I should mention that when I work with clients, we don't really even look at The withdrawal rate, it's something we can find after the fact, after we've done some more robust planning, but we don't start with a withdraw rate, it's just something we might check out of curiosity. As a quick refresher, a withdrawal rate is a way of looking at how much you're pulling out of your savings and investments that are earmarked for retirement. Perhaps. The most famous and the most notorious is the so called 4% rule, which is really more of a research finding, so it's not a rule that you would necessarily follow, although some people talk about it that way. It's based on some research that was done by Bill Bengen where he looked at how much could you withdraw from a portfolio over a typical 30 year retirement horizon, and let's say you have a 50 50 stock and bond portfolio.

Well, what it turned out was in his research at the time, you could take out 4% of your starting portfolio and adjust it for inflation and not run out of money in any of those worst case scenario historical periods that lasted 30 years. Now, since then, the rule has been debated and criticized and refined, and people talk about things like, what about the current environment? Or what if I diversify more? How might that look? And a lot of people just love or hate the 4% rule. Either way, I don't think it's the best way to go about it, but it's important to understand how it works. So just for simplicity's sake, let's use round numbers that are easy to multiply in our head, and we'll say, let's say you have 100,000, or for each 100,000 of savings that you have at retirement, we would say You can pull 4% of that out per year, and we start with your first year, 4% of 100,000 is 4,000. So that's your Year One withdrawal, now you're going to adjust this for inflation each year, so in the subsequent here, If inflation is anything above zero, you're going to pull out more than that initial 4000 and with each passing here, you're going to adjust your withdrawals, you continue to take those inflation adjusted withdrawals each year, regardless of what happens with the markets or how high inflation is for at least that's how it worked in the original research, so that's a basic overview of a withdrawal strategy like the 4% rule, but just as one example of something that might be missing in that analysis because it's pretty over simplified is taxes.

So for example, are you pulling money out of pre tax accounts that you're going to go income tags on like a traditional IRA, or are you pulling from taxable brokerage account or Roth accounts? They wouldn't necessarily have as much tax, so depending on where the money comes from, that 4000 or 40000, if you have a million dollars is going to offer you more spending money or less…

Now again, at a 40000 income, the taxes might not be too burdensome, but you need to know that there are probably some taxes due, so that's going to affect your budget, another issue with withdrawal rates or the 4% rule, for example, is that you might not spend as much as you could, and that might mean you're missing out on opportunities, making memories or doing things you want to do, or retiring at a later date then you need it to… Historically, there were quite a few runs where you ended up with a lot more money than you started out with, so we assume you started with 1 million dollars, you did a 4% withdrawal rate, and you had more than 2 million at the end of your life, 45% of the time, your money doubled over your retirement years, or in some cases, you might have died with more than 5 million.

That's great if your goal is to give money away at death, but if your goal is to maximize your enjoyment of your assets during life, then a simplified withdraw rate might not let you do that. This would be a perfect time to mention that past performance does not guarantee future results, and this is just a short video, so friendly reminder, please do a lot more research before you make any decisions, decide to take any action or not, because this stuff is really important. So please read that carefully, and by the way, I'm Justin Pritchard and I help people plan for retirement and invest for the future, so in the description below, you're going to find more resources on this topic, some discussions about withdrawal rates and some calculators that help you work with withdrawal rates, if you want to go that route and look at some alternatives, I think you'll find all of that helpful.

When you make a more robust income plan, you might have a withdrawal rate that varies over time, so it might start relatively high, perhaps you're withdrawing at a relatively high rate in the early years of retirement and spending down some assets, and that might be something you do as you wait for Social Security benefits to start, perhaps you're going to delay Social Security, maybe you want that time to make a little bit of room so that you can do Roth conversions or fill up some tax brackets, or maybe you're just trying to maximize what your Social Security benefit is, there's some really good reasons for doing this, for example, maybe there's going to be a survivor involved, and you want to make sure that that benefit is as high as possible because once one spouse dies, for example, the surviving spouse would be left with just one Social Security income, so perhaps it's important to have that be as high as possible, and here's an example of how that could look, so we can just check somebody's withdrawal rate.

And in this case, they aren't going to start Social Security until age 70, so they have started out with a relatively high rate here, then it drops off as other income sources kick in, they're in the low threes here for a while, and then when Long term care expenses come up, you're back to a high withdrawal. We can also see how it looks kind of visually with the asset levels, so again, at retirement here, maybe they're going to wait until 70, they're going to spend down some assets for a while, and then that curve… And by the way, this can be kind of nerve racking to watch your assets decrease over time, but if you have a plan in place and you've got those retirement income sources that can perhaps help you have the confidence they, again, here spending down assets until the Social Security and pension sources kick in, and then the withdrawal rate decreases dramatically, now, not everybody has a pension plus Social Security, that's actually going to help them increase their assets once those income sources kick in, but some people are fortunate, and that's what retirement looks like for them.

One other issue with withdrawal rates is that your spending can change over time, so as just one example, maybe you're going to buy a car periodically, and so that spikes your withdrawal rate every couple of years, so how do you deal with that? Or if we look at research on retiree spending, not everybody spends a flat inflation adjusted amount each year, in fact, for some retirees, you might have them spending at roughly inflation minus 1%, of course, that ignores those healthcare expenses which continue to increase at a pretty fast rate, probably faster than general inflation is a good way to model that, but other expenses might not increase, so if you own your home and you don't drive too much, for example, you might not be experiencing a lot of inflation. In fact, David Blanchett's research called the retirement spending smile actually shows retirees spending at roughly inflation minus 1%.

Or another way to look at this is your retirement spending stages. Sometimes people call this the go go, the slow go and the no go years. So right after you retire, you might be spending at a relatively high rate, these are your go go years, you've just finished working, you've saved all your life, you want to travel and have fun, and so you're going to do that while you're still young and healthy, but then you get into the slow go years, your spending might slow down a little bit, you've done a lot of the travel, you're spending more time just with friends or family or whatever the case may be, and then we get into the no go years where a lot of your leisure and entertainment recreation spending are going to decrease, but that healthcare spending ramps back up in the no go years, so if we're thinking of that in terms of withdrawal rates in the go go years, you're at a relatively high rate, slow go years, not quite as high, and the no go years, you're back into a relatively high rate, so I hope now you have a richer understanding of withdrawal rates.

If that helped, please leave a quick thumbs up. Thanks, and Take Care..

Read More

Best Gold IRA Companies 2024

Jason 0 Comments Retire Wealthy Why Gold IRA