Tag: 401(k)

How 2024’s Record Retirement Numbers Could Spark a Recession | WSJ

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

– [Narrator] You're looking at

a chart of the US population, and these are the baby boomers. This year, a record number of them will reach

traditional retirement age. By 2030, they'll all be 65 or older. This is creating a fiscal problem because fewer taxable

workers means less money for social security. – If Congress does nothing,

we're gonna hit a major crisis.

– [Narrator] Here's how

this demographic shift threatens the future of one of the country's most

important government programs and what can be done to fix it. Baby boomers or those born between 1946 and 1964 have been propping

up the US economy for decades. – Their mere numbers

contributed for a long time to rapid economic growth and because every worker

contributed social security that made social security

look very healthy. – [Narrator] But as boomers

started exiting the workforce in 2008, the number of

retirees grew rapidly. – Not only do you have more

retirees collecting benefits for more years, you

have fewer young people entering the workforce

because birth rates were lower for their parents' generation, and that creates a squeeze

on both directions.

Higher expenses from all

those retirees living longer, lower payroll tax revenue from fewer people entering the labor force because of those declining birth rates. – [Narrator] This puts a lot

of pressure on social security and without policy change, projections show the trust

funds will be depleted in 2034. – There's a misconception out there that when the social security

trust fund is exhausted, the system is somehow

bankrupt and there's no money. Social security is an integral part of the federal government, and as long as the federal

government is not bankrupt, social security is not bankrupt. – What's really happening is

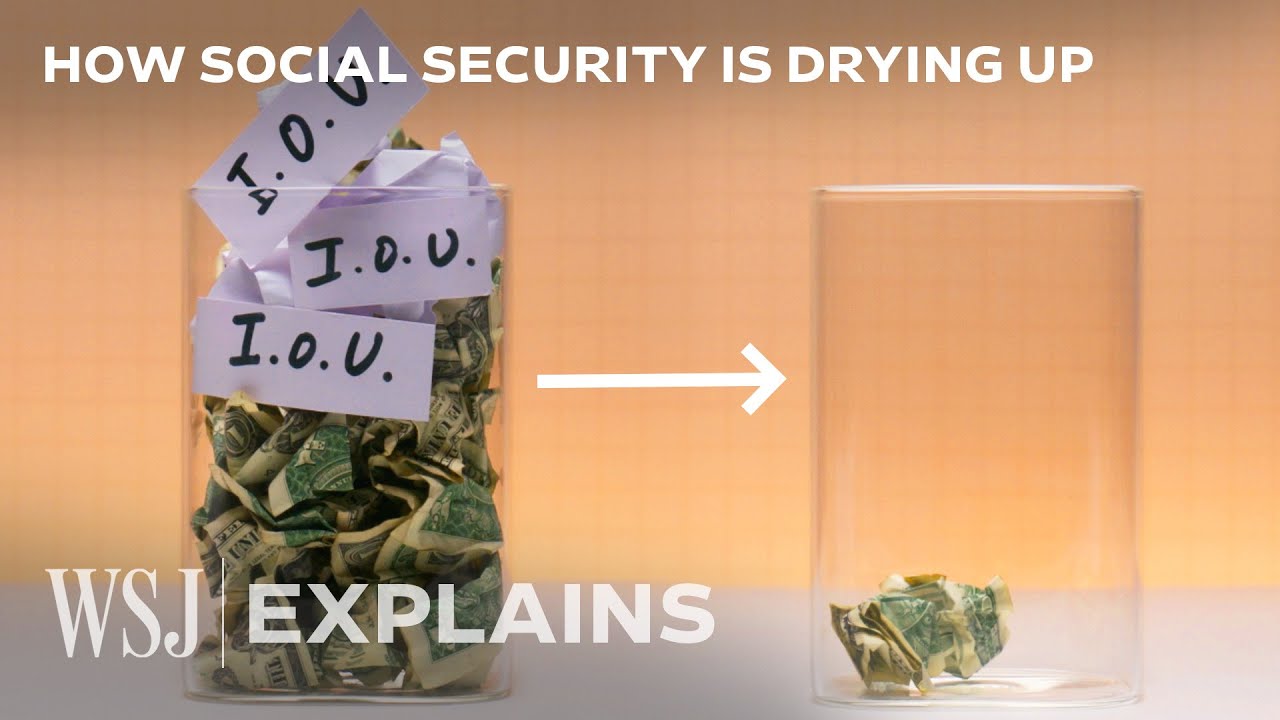

the program is running out of treasury bonds, which are basically IOUs

from the government. For many years, social security

was taking in more money than it needed to pay out in

benefits, so it lent money to the government to

use for other programs, and it got IOUs in return. – Around 10 years ago though,

that situation flipped around.

For the last decade, we've been

paying out more in benefits than we've been collecting

in social security revenue. – [Narrator] But because the program had so many IOUs stashed

away from previous years, it's been able to keep

paying benefits in full by cashing in on those IOUs. – Right now, there's

roughly $3 trillion in IOUs, but each year that $3 trillion stash gets a little bit smaller. By the year 2034, all of the

IOUs will have been cashed in. – That means retirees would see overnight about a 25% benefit cut. – [Narrator] This number will

likely increase as the number of workers per retiree continues to fall. – Simply because we're not about to go bankrupt doesn't

mean there's no problem.

There very much is a problem. – [Narrator] Studies

show that the majority of Americans rely on these

monthly benefits checks for retirement income. According to census bureau

data, about 50% of people between 55 and 66 years old

have no retirement savings. – Can you imagine right now if you had to take a 25% reduction

in your take home pay, you still have to pay rent. You gotta buy groceries,

you gotta pay utilities. – It's especially important for those who don't have college degrees, people on the lower end

of the income spectrum. – [Narrator] Fichtner says, when retirees have less retirement income, they also generally spend less money. – That means less economic activity. That means less employment because employers have to lay off people 'cause no longer is that money coming in. It's a ripple effect that could be basically a

senior induced recession. – But social security is only

meant to replace a percentage of a worker's pre-retirement income based on lifetime earnings. So as much as 78% for very

low earners to about 42% for medium earners and

28% for maximum earners. – This is three legged stool

we talk about all the time.

It's supposed to be social

security is one leg, your employer provided pension is a second leg and your

personal savings a third. Well, social security

is financial challenges. We don't have pensions really anymore. About 10% of the population has pensions and then it's hard to save on your own when you've gotta pay off student loans and housing costs are so high. – [Narrator] About half of Americans do have retirement accounts

like 401Ks and IRAs, but those are all subject to market risk. – I hear a lot, well,

those are 65 year olds.

Why do I have to worry

about the boomers today? Well, this impacts every

generation that's coming up behind. – They might not be asked to pay a slightly higher payroll tax. More important, they might be asked to work a little bit longer. – [Narrator] And like most

things in the economy, social security's funding

shortfall isn't an isolated issue. – It's one of the reasons

the federal budget deficits is as large as it is. It means that we have to borrow money, which means issuing bonds. That tends to put up

pressure on interest rates, which means it's harder to afford a house. It means that Congress might have to cut spending on other

programs like the military or the environment in order to make sure that there's enough money

for social security. – [Narrator] So what needs to

happen to put social security on more sound footing? Congress needs to pass a law. – Congress has stood still and not enhanced social

security since Richard Nixon.

– [Narrator] When and what kind of law, that we still don't know. There's been a number of proposed

solutions over the years. – This legislation demands that the wealthiest people in this country start paying their fair share of taxes, – But policymakers generally

disagree on whether to raise taxes or cut benefits. – You'll have two approaches

to how to solve this problem, and you're not gonna do it. – There's probably no single magic bullet, which will put social security

on a long-term footing. Instead, Congress is

probably going to have to look at a variety of steps which will collectively fix the problem.

– [Narrator] But economists

don't expect action to be taken anytime soon. – Everybody, including on Capitol Hill, knows that social security has a problem. Nobody, especially those in Capitol Hill, are prepared to do anything about it. – As we all apparently

agree, social security and Medicare is off the books now, right? They're not to be smart.

(clapping and cheering) – We all would wish that

politicians would show the political courage

necessary to tackle this now and not wait until the 11th hour. Benefits and changes to retirement programs

take a while to phase in. One of the last major reforms we had for social security were the 1983 reforms. – [Narrator] Those amendments

raised the retirement age to 67, but it took nearly

40 years to phase them in.

– There is a 10 year window, but we don't have 10 years to act. – There has to be some kind

of a legislative solution that comes along between now and then. By law, the program can't

borrow anywhere else. The program's too important,

too popular for it to basically be allowed

to run out of money..

3 Retirement Savings Tips Before Year-End (Full Webinar)

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Welcome, everyone, thank you for joining us today. My name is Ewelina Caplap, Wealth Management operations manager at Coastal Credit Union, where we bank better to live better. Today, we will be sharing with you three retirement savings tips before year end. So hopefully today you will come out of this session with some great action items. Joining me today are David Burk, CFS financial advisor, and Drew Snider, CFP, director of financial planning here at Coastal Credit Union. Welcome to you both. So before we get into our exciting conversation, we will very quickly cover our disclosure slide. Coastal Credit Union contracts with CUSO Financial Services to offer investment products to its members, which can fluctuate with market activity and potentially have some risk. So getting into our exciting conversation today about three retirement savings tips for year end. At this time, let's talk about tip one. Tip one, Roth IRAs. We hear about Roth IRAs quite a lot and the potential tax free income they provide. David, why don't you start us off with a little bit about what this tip is? Thanks, Ewelina.

A Roth IRA is an IRA that you're actually using after-tax dollars to invest in a credit union or an investment Roth IRA and letting that grow tax deferred so that after age 59 and a half, you'll be able to withdraw money out of that account that is 100 percent tax free. That's a huge financial and tax benefit that you should certainly consider before year end. Why don't you add a little bit more to that, Drew? Yeah, the Roth IRA is is definitely the greatest savings tool we have for retirement. As the illustration shows, the seed for our tree is what's getting taxed. And then you grow this beautiful tree with all this great money on it and you get to take the money off and you don't pay taxes on the money.

So it's fantastic and everyone should consider if they can do it or not. The beauty of looking at a Roth IRA going into December is you have a vision of what your income is for the year and you have limitations on contributions based on what your income was for twenty twenty one. So if your income is basically under about one hundred twenty five thousand dollars as a single person or one hundred ninety eight thousand dollars as joint filers, you should definitely be looking at a Roth IRA and coming into the credit union and talking to us to see if it'll work for you. That's excellent. What a great first tip to consider taking care of before the year end. So we're now going to move over to tip number two, and we're going to talk about some 401(k)s. What can you tell us here, David? 401(k)s are offered typically through an employer or as an employer sponsored retirement plan. They've been around for quite some time now, and many employees should be taking full advantage of this retirement savings.

And again, since we're now getting towards the end of the year, it's always a benefit to evaluate your income at this year, like Drew mentioned in the previous slide. But then also what your income will be next year and give yourself a savings raise of trying to increase your savings. Drew, I'll let you expand more about the comparison of Nick versus Maria and what their savings has done over time. Sure, I'd be happy to. This is a very simple graphic of two individuals who make the same amount of money and started off saving the same amount of money, the same percentage to their 401k plan. Nick maintained that savings rate, whereas Maria, each year, increased her savings rate by one percent or her contribution rate by one percent to her 401k plan until it maxed out at 15 percent.

And you can see that over time, Maria had quite a bit more money. This is after 30 years. She had twice as much money for retirement as did Nick. And you know what? You don't really need to concentrate on anything other than the fact that that right bar looks a lot bigger than the left bar. So with proper planning, we can help our viewers get there. Yeah, just one more comment here. Before year end, everyone should take a look at their 401k statement and see if they maximized. If they're trying to maximize the amount that they can contribute, they should take a look at that and see if they've been able to do that this year, because a lot of people may think that they are maximizing their contributions when in fact they haven't.

Right? Good point. And another thing, I'm not sure if we mentioned it, if you have a Roth 401k option on your plan, if we're talking about a Roth IRAs, certainly Roth 401k option is something that our viewers should be looking into. Can either one of you speak to that for a minute? Yeah, that's an interesting comment, Ewelina, because that's still relatively new in the marketplace and offered through employer 401k plans, but the numbers are astounding how few people are really taking full advantage of that Roth opportunity in their 401k. And what that means is, you can actually contribute more towards your Roth 401k than you can a Roth IRA outside of your employer-sponsored plan. Plus, your income is not a restrictive factor in being able to contribute to the Roth 401K plan. And just add to that, I would encourage anybody, even high income people who really do like the tax deduction that they're getting from their traditional 401k contributions. It's not an either/or situation. You know, if you're not doing either traditional or Roth, you can do some in both.

Personally, I do some in both of mine. I do some in the traditional and I do some in the Roth in my contributions. I do the same thing on my own planning as well. Well, certainly a lot to take in and consider for year end. So we're going to move on to our final tip. Tip three. Health savings accounts, right? HSAs. And who doesn't like the sound of triple tax savings? So, David, what don't you tell us a little bit about that first? The triple tax saving on a health savings account is phenomenal, and many people have completely overlooked this opportunity for their own household and and being able to save tax free money. So what ends up happening. If your employer offers you a high deductible health account, then you can participate in an HSA.

And what you're able to do is contribute on an individual basis or as a family, and that money can be tax deductible as far as the contribution. Once that money is in your HSA, it grows tax deferred. And then when you're ready to start withdrawing money from an HSA for a qualifying medical or health care expense, it's one hundred percent tax free as a distribution. And I want to comment here. As as you come to the year end, some employers are going to contribute some money to your HSA for you. You can add the rest up to the maximum. And you have until April 15th to do that. But the year end is a great time to take a look to see how much your employer has put into that plan for you. And then what is the calculation? What's the amount that you can add to it? Because you can reduce your taxes in your 2021 tax return, you get tax deferral and you can take the money out tax free for qualified health care expenses.

Excellent. So it sounds like there's a lot to get done here working with Team Coastal. So who are we right? Who is Team Coastal? Drew, can you talk to us about how we can help our viewers in meeting these three tips? Putting them into action? Yeah. Whether you're talking to Coastal Wealth Management about these concepts that we talked about today, or if you go into the branch, the credit union, you're going to get a team of experienced people that are going to be able to help you make your contributions, maximize your retirement. At Coastal, they're going to talk to you about your savings account options and Wealth Management.

If you have a more longer term perspective, we're going to show you some investment options for your IRAs. And then, you know, one thing about Coastal Wealth Management is, you know, we have lots of options to help you to find a great solution that you're comfortable with. That fits your risk tolerance and your needs, and we're all working together. So whether you talk to someone at the branch and you tell them, Hey, I'd like to get a better rate of return, than you're offering in that savings account, they're going to bring us into the conversation with Wealth Management so we can talk to you about how we can help. So we're all working together at Team Coastal. And then obviously, if you want to do a financial plan with us, we'd be happy to help you with that. Absolutely. And speaking of that financial plan, for our viewers, if they are not aware, it is a complimentary financial review to meet with our team and discover all the options available to you with Team Coastal, whether that be something that our retail team can help you or our Wealth Management department specifically, we all work together and can hopefully help you reach your goals.

Schedule your complimentary Financial Review with us today. You can call us at 919-882-6655. You can certainly send us an email [email protected]. And of course, you can find us online as well. There are some action items to take here with these three tips before year end. We're happy to help you with that. Thank you again… David Burke, CFS financial advisor, one of our dedicated advisors for being with me here today, and of course, Drew Snider, our financial planning director here at Coastal Credit Union. Thank you for your time today and thank you to our viewers for joining us.

And reach out to us. We'll be happy to help you..

Read More

3 Retirement Savings Tips Before Year-End (Full Webinar)

Jason 0 Comments Retire Wealthy Retirement Planning Tips for Retiree's

Welcome, everyone, thank you for joining us today. My name is Ewelina Caplap, Wealth Management operations manager at Coastal Credit Union, where we bank better to live better. Today, we will be sharing with you three retirement savings tips before year end. So hopefully today you will come out of this session with some great action items. Joining me today are David Burk, CFS financial advisor, and Drew Snider, CFP, director of financial planning here at Coastal Credit Union. Welcome to you both.

So before we get into our exciting conversation, we will very quickly cover our disclosure slide. Coastal Credit Union contracts with CUSO Financial Services to offer investment products to its members, which can fluctuate with market activity and potentially have some risk. So getting into our exciting conversation today about three retirement savings tips for year end. At this time, let's talk about tip one. Tip one, Roth IRAs. We hear about Roth IRAs quite a lot and the potential tax free income they provide. David, why don't you start us off with a little bit about what this tip is? Thanks, Ewelina.

A Roth IRA is an IRA that you're actually using after-tax dollars to invest in a credit union or an investment Roth IRA and letting that grow tax deferred so that after age 59 and a half, you'll be able to withdraw money out of that account that is 100 percent tax free. That's a huge financial and tax benefit that you should certainly consider before year end. Why don't you add a little bit more to that, Drew? Yeah, the Roth IRA is is definitely the greatest savings tool we have for retirement.

As the illustration shows, the seed for our tree is what's getting taxed. And then you grow this beautiful tree with all this great money on it and you get to take the money off and you don't pay taxes on the money. So it's fantastic and everyone should consider if they can do it or not. The beauty of looking at a Roth IRA going into December is you have a vision of what your income is for the year and you have limitations on contributions based on what your income was for twenty twenty one.

So if your income is basically under about one hundred twenty five thousand dollars as a single person or one hundred ninety eight thousand dollars as joint filers, you should definitely be looking at a Roth IRA and coming into the credit union and talking to us to see if it'll work for you. That's excellent. What a great first tip to consider taking care of before the year end. So we're now going to move over to tip number two, and we're going to talk about some 401(k)s. What can you tell us here, David? 401(k)s are offered typically through an employer or as an employer sponsored retirement plan.

They've been around for quite some time now, and many employees should be taking full advantage of this retirement savings. And again, since we're now getting towards the end of the year, it's always a benefit to evaluate your income at this year, like Drew mentioned in the previous slide. But then also what your income will be next year and give yourself a savings raise of trying to increase your savings. Drew, I'll let you expand more about the comparison of Nick versus Maria and what their savings has done over time. Sure, I'd be happy to. This is a very simple graphic of two individuals who make the same amount of money and started off saving the same amount of money, the same percentage to their 401k plan. Nick maintained that savings rate, whereas Maria, each year, increased her savings rate by one percent or her contribution rate by one percent to her 401k plan until it maxed out at 15 percent.

And you can see that over time, Maria had quite a bit more money. This is after 30 years. She had twice as much money for retirement as did Nick. And you know what? You don't really need to concentrate on anything other than the fact that that right bar looks a lot bigger than the left bar. So with proper planning, we can help our viewers get there. Yeah, just one more comment here.

Before year end, everyone should take a look at their 401k statement and see if they maximized. If they're trying to maximize the amount that they can contribute, they should take a look at that and see if they've been able to do that this year, because a lot of people may think that they are maximizing their contributions when in fact they haven't. Right? Good point. And another thing, I'm not sure if we mentioned it, if you have a Roth 401k option on your plan, if we're talking about a Roth IRAs, certainly Roth 401k option is something that our viewers should be looking into. Can either one of you speak to that for a minute? Yeah, that's an interesting comment, Ewelina, because that's still relatively new in the marketplace and offered through employer 401k plans, but the numbers are astounding how few people are really taking full advantage of that Roth opportunity in their 401k.

And what that means is, you can actually contribute more towards your Roth 401k than you can a Roth IRA outside of your employer-sponsored plan. Plus, your income is not a restrictive factor in being able to contribute to the Roth 401K plan. And just add to that, I would encourage anybody, even high income people who really do like the tax deduction that they're getting from their traditional 401k contributions. It's not an either/or situation. You know, if you're not doing either traditional or Roth, you can do some in both. Personally, I do some in both of mine. I do some in the traditional and I do some in the Roth in my contributions.

I do the same thing on my own planning as well. Well, certainly a lot to take in and consider for year end. So we're going to move on to our final tip. Tip three. Health savings accounts, right? HSAs. And who doesn't like the sound of triple tax savings? So, David, what don't you tell us a little bit about that first? The triple tax saving on a health savings account is phenomenal, and many people have completely overlooked this opportunity for their own household and and being able to save tax free money.

So what ends up happening. If your employer offers you a high deductible health account, then you can participate in an HSA. And what you're able to do is contribute on an individual basis or as a family, and that money can be tax deductible as far as the contribution. Once that money is in your HSA, it grows tax deferred. And then when you're ready to start withdrawing money from an HSA for a qualifying medical or health care expense, it's one hundred percent tax free as a distribution. And I want to comment here. As as you come to the year end, some employers are going to contribute some money to your HSA for you. You can add the rest up to the maximum. And you have until April 15th to do that. But the year end is a great time to take a look to see how much your employer has put into that plan for you. And then what is the calculation? What's the amount that you can add to it? Because you can reduce your taxes in your 2021 tax return, you get tax deferral and you can take the money out tax free for qualified health care expenses.

Excellent. So it sounds like there's a lot to get done here working with Team Coastal. So who are we right? Who is Team Coastal? Drew, can you talk to us about how we can help our viewers in meeting these three tips? Putting them into action? Yeah. Whether you're talking to Coastal Wealth Management about these concepts that we talked about today, or if you go into the branch, the credit union, you're going to get a team of experienced people that are going to be able to help you make your contributions, maximize your retirement. At Coastal, they're going to talk to you about your savings account options and Wealth Management. If you have a more longer term perspective, we're going to show you some investment options for your IRAs. And then, you know, one thing about Coastal Wealth Management is, you know, we have lots of options to help you to find a great solution that you're comfortable with.

That fits your risk tolerance and your needs, and we're all working together. So whether you talk to someone at the branch and you tell them, Hey, I'd like to get a better rate of return, than you're offering in that savings account, they're going to bring us into the conversation with Wealth Management so we can talk to you about how we can help. So we're all working together at Team Coastal. And then obviously, if you want to do a financial plan with us, we'd be happy to help you with that. Absolutely. And speaking of that financial plan, for our viewers, if they are not aware, it is a complimentary financial review to meet with our team and discover all the options available to you with Team Coastal, whether that be something that our retail team can help you or our Wealth Management department specifically, we all work together and can hopefully help you reach your goals. Schedule your complimentary Financial Review with us today. You can call us at 919-882-6655. You can certainly send us an email [email protected]. And of course, you can find us online as well.

There are some action items to take here with these three tips before year end. We're happy to help you with that. Thank you again… David Burke, CFS financial advisor, one of our dedicated advisors for being with me here today, and of course, Drew Snider, our financial planning director here at Coastal Credit Union. Thank you for your time today and thank you to our viewers for joining us. And reach out to us. We'll be happy to help you..

Read More

Are 401(k)s a Financial Silver Bullet?

Jason 0 Comments Retire Wealthy Retirement Planning

It’s hard to find something everybody agrees

on. Crunchy or smooth? Smooth. Mac or PC? Fries or onion rings? Fries. But if there’s one financial instrument

that seems universally beloved, it’s got to be the 401(k). Everybody loves ‘em! People delay saving for a home, building an

emergency fund, or even paying off high-interest debt in pursuit of this conquering hero: the

tall, dark, and handsome 401(k). My hero… There’s a whole lot to love with the 401(k). So saddle up and take a ride to find out what

makes this cowboy the darling of investors everywhere! The year was 1980, and The Revenue Act of

1978 was finally going into effect.

And deep in the bill was a tiny provision;

Section 401, Subsection K. Largely overlooked, Section 401(k) allowed employees to defer

taxes on bonuses and stock options — basically a way for rich executives to make more and

pay less tax on it. But everything changed in 1981 when the IRS

ruled that employees could also contribute from their SALARY. This was music to employer’s ears! Managing all those employee pensions was expensive,

complicated, and downright risky! Maybe this new fella, 401(k), could replace

the dusty old pensions of our grandpappies. Before long, 401(k) fever was spreading like

wildfire! By 1996, 401(k) accounts held over a trillion

dollars! How does it work? Fundamentally, a 401(k) is an employer-sponsored

investment account.

It lets you invest part of your paycheck and

receive a tax benefit for doing so. Like company-provided insurance programs,

you have to opt-in to participate. The most attractive feature is the “employer

match”. Translation: if you save for your future,

the boss rewards you with “free” money, matching your contribution dollar for dollar,

up to a limit. Around half of 401(k)s offer an employer

match and this “free money” can come to thousands of extra dollars! Then there’s the sweet tax breaks.

Depending on the type of 401(k), your contributions

could be “pre-tax”, meaning it lowers your taxable income for the year. OR, you can pay the tax now, and allow that

money to grow tax-free. The more you save, the less taxes you pay. Looking pretty spiffy over there, Mr. 401(k)! Oh — and don’t forget that your contributions

are being invested in stock and bond funds. We have Two Cents episodes about those if

you’re not sure how they work. Now you can just sit back and watch compound

interest fatten your herd! Free money, big tax breaks, and investment

growth! What’s not to love?! Hold your horses there, partner. While the 401(k) has a lot going for it, there

are a couple burrs under the saddle.

Like the risks of managing your own investment

portfolios instead of leaving it to the professionals. As 401(k)s soared in popularity during the

80’s and 90’s, billions of dollars flowed into risky sectors like tech-stocks. And when things came crashing down — like

they did twice in the 2000’s — many working folks were left adrift like a tumbleweed in

the wind. And did you know that “Mr 401(k)” doesn’t

work for free? A study by TD Ameritrade found that 73% of

participants didn’t know how much their 401(k) costs, while 37% weren’t aware they

were paying fees at all! Investment firms regularly rack up hefty fees

since nobody’s paying attention — with the average being around 1.4%! And remember that juicy employer “match”

we mentioned earlier? Well, that might not end up being yours thanks

to “401(k) vesting”.

Even though funds might appear in your account,

they’re only yours once you become “vested” — often 3 to 5 years after you get hired! With the vast majority of millennials only

expecting to stay in a job for a few years at the most, that’s a lot of “free money”

that never gets collected. Despite their perks, and general popularity,

401(k)s have left a societal legacy that’s, well, ugly. See, 401(k)s were originally designed to be

a supplement to worker pensions. For most of the 20th century, it was common

for workers to stay with a single employer for most of their lives. And for that loyalty, their company offered

a defined benefit pension for the worker’s golden years.

These plans offered steadiness and security,

with the employer watching over everyone’s plans — from the janitor to the CEO. By their peak in 1980, 38% of all private

sector workers had an employer pension. Today, thanks to the 401(k), only 13% of private

sector workers have a pension. And while 401(k)s have their perks, they're just not as stable or reliable. 401(k)s are also “opt-in,” which means

you aren’t automatically enrolled. Left to their own devices, many employees simply aren’t saving enough — if they’re saving at all. Of the 79% of workers eligible to save into

a 401(k), only 41% opt to participate. The National Institute on Retirement Security

finds that the median retirement savings balance is just $3,000 for all working-age households

and a mere $12,000 for those near-retirement! Most financial experts recommend a personal

retirement savings rate between 10 – 15%.

The real rates are between 1 and 3%. The 401(k) was designed to be the side-dish,

not the main course. Saddling workers with the “opportunity”

to manage their own retirements has created a national crisis in retirement preparedness. But the good news is that if you know its

place, and use it wisely, a 401(k) can be a great part of your financial toolkit. Since pensions are going the way of the horse

and buggy, you’ll need your 401(k) to be galloping double-time to keep from being left

in the dust.

Take advantage of it and you’ll be riding

into the sunset instead of off a cliff. And that’s our two cents! If you've been transitioned from a pension to a 401(k) tell us about experience in the comments!.

Should You Roll Over Your 401(k)?

Jason 0 Comments Retire Wealthy Retirement Planning

To roll or not to roll. THAT is the question. Well, that’s the question if you have a

401(k) from a previous employer. If you’ve changed jobs and are wondering

what to do with your 401(k)account, you have four choices: leave it where it is, roll it

into your current employer’s plan, roll it into an IRA, or cash it out. There’s no one right answer for everyone,

but there are a few key considerations that can help you decide: fees, access to your

money, and investment choices.

First up: fees. 401(k) accounts can carry a number of fees,

which differ based on the provider. When it comes to fees, the most important

thing to understand is what you’re paying and whether the features of the plan justify

it. The most common is management fees, which

are associated with the mutual funds or ETFs typically available in retirement accounts.

These are usually expressed as percentages called expense ratios. But there are also plan fees. 401(k)s, for

example, can be loaded with both upfront and hidden costs like admin fees, audit fees,

and asset fees. While these fees can be avoided or reduced

by investing in an IRA, this is not always the case. It’ll ultimately depend on which

brokerage you choose, what funds you invest in, and how often you trade. The thing to keep in mind is while fees can

add up and eat into your retirement savings, it doesn’t mean the cheapest solution is

always the best. Depending on your needs, access to advice, retirement planning tools,

or better investment choices may be worth paying the higher fees.

Another consideration when deciding whether

to roll is when you think you’ll need to access the money. Depending on your age, withdrawal penalties

and conditions may apply. If you think you’ll need to withdraw funds

from your retirement account before the standard 59 ½ age requirement, you might consider

rolling into your current 401(k). Thanks to an IRS rule known as the rule of

55, if you leave a job any time during or after the calendar year in which you turn

55, you can start taking money out of your current 401(k) penalty-free for any reason. Just know the 59½ age requirement still applies

for any money in a previous employer’s 401(k), which means you’ll pay the penalty if you

try to withdraw money early. On top of that, some 401(k)s also allow you

to take out a loan of up to $50,000 from your current account. And you’ll have up to five

years to pay it back. Keep in mind that with an IRA, you can only

withdraw money early for qualified expenses like medical bills and education costs. You

can also withdraw up to $10,000 for a first home purchase. Any other money withdrawn before age 59 ½

must be repaid within 60 days or you’ll face penalties.

While it’s generally best to keep your retirement

savings invested, your unique circumstances may require you to access your money early,

and this may impact your decision about rolling over.

The third factor to consider is the type of investments each account offers. 401(k)s tend to offer a limited number of

investments chosen by a plan administrator, often mutual funds or exchange-traded funds. These choices sometimes come with high fees, but there are some plans that do offer a variety

of low-cost investments as well as investments that may be unavailable elsewhere. IRAs, on the other hand, tend to offer access

to a much wider variety of investment choices, including individual stocks. One more thing regarding investment choices:

did your previous employer issue company stock through your 401(k)? If the answer is yes

and the stock has grown in value, rolling over could mean serious tax ramifications. If this situation applies to you, talk to

a tax professional to make sure you’re not setting yourself up for a tax surprise next

April.

So there you have it fees, access to your

money, and investment choices. These are three of the biggest considerations

when it comes to deciding whether to roll over a 401(k) from a previous employer. The right choice for you depends on your unique

financial situation. A little research now can help ensure you’re able to thrive in

your golden years..

Suze Orman Gets You Ready For Retirement | Money

Jason 0 Comments Retirement Planning

I am the one and only Susie Orman, and my goal is to make you as independent from financial advisors as possible, because you are never going to be powerful in life until you are powerful over your own money. And my job is to make sure you can achieve just that. So rather than asking more from your money that it can't give you, you have to ask less of your spending habits from yourself which means you have got to get rid of all credit card debt. All debt. Total debt of car loans, mortgage debt, all debt that you have has to go. So one thing that you have to look at is if you have a debt, that is your sign that you can't afford to retire. Maybe you retire from the job that you currently have, but then you have to get some side hustles or something. So my best advice to you is start living below your means but within your needs.

How do you do that? From this day forward, every time you go to make a purchase, ask yourself a question, 'Is this a want or is this a need?'. If it's a want, please don't purchase it. If it's a need, you have to buy it. It's just that simple. You know, a lot of you, when you're approaching retirement, you look at your portfolio and usually your portfolio is this: you have a 401 9k), 403 (b), a Thrift savings plan if you work for the government or whatever, it may be, the military. And now you've retired and now normally you would then do an IRA rollover with that money. But now you're 'Oh my God, what should I do? I never invest in money before, really. I've just put money in every single month into these mutual funds. And now I don't know what to do.'. If you are going to be withdrawing money from your retirement account to pay for your everyday expenses, you have to know that you have — ready for this, everybody — at least three years of expenses in cash, earning you a high interest rate or whatever the highest interest rate is that you can get.

The rest, at this point in time, should really be diversified into high-yield dividend-paying either stocks or exchange-traded funds. If you need really short term money and you want to get a higher interest rate for very short term money, right, I don't have a problem with bills. And, you know, I myself will put a serious sum of money protected in bills because if you're investing more than $250,000, then you really have to go to a variety of banks in order to get FDIC insurance — or even credit unions.

So if you have a large sum of money of $1 – $3 million that you just want liquid, then I use Treasury bills for that. I don't have a problem with that at all. And they keep rolling over but I know that they're guaranteed by the taxing authority of the United States government. If we're talking now, though, about amounts that are $250,000 or below, I think that you're far better off, right here and right now, putting the money in a high-yielding savings account.

So for smaller amounts of money, savings account. For $250,000 or above that you want liquidity and the highest interest rate, I don't have a problem with Treasury bills. You don't have the documents in place today to protect your tomorrows. You don't have a will. You don't have a living revocable trust. You don't have an advance directive and durable power of attorney for health care. And you don't have a power of attorney for finances. You need those things not just to make sure that your assets pass freely to your beneficiaries. You need those things for you. So here you are now and your spouse has died. Who, as you get older, who's going to write your checks for you? Who's going to pay your bills for you? If you get sick, you have an incapacity, who's going to do that? So it's very important that you get the documents that are correct.

Long-term care insurance, if you can afford it, will absolutely protect your little nest egg if one of you ends up in a nursing home. One out of three of you will spend some time in a nursing home after the age of 65. So look around and if you decide to buy long-term care insurance, the perfect age to buy it is really in your 50s. But here's the key. You better know that you can afford a long-term care insurance premium because they're not cheap. From the age of when you buy it all the way until at least 84 because it makes no sense for you to purchase it. Pay for it in your 50s, in your 60s. Now here you are in your mid 70s, you can't afford it anymore and then you drop it. You're better off just not buying it at all. Let me just put it to you bluntly. You are to stay as far away from a reverse mortgage as you possibly can. There is not one situation out there where you should be getting a reverse mortgage.

A reverse mortgage is based on the interest rates that are in effect right here and now. It's based on your age. And it just makes no sense. If you own a home and you can't afford to stay in that home — with real estate prices as high as they are — you could just sell your house right now and either seriously downsize, or there is nothing wrong with renting..

Read More

Recent Comments